- Investors digested a bout of weak consumer survey results this week and speculated the Federal Reserve (Fed) could shift their focus from inflation to fighting deteriorating sentiment, increasing market expectations for Fed cuts later this year

- Consumer confidence experienced the sharpest monthly decline since August 2021, falling to 98.3 in February from 105.3 in January and underperforming expectations of 102.5 as inflation pressures continue to weigh on consumers

- Fourth quarter GDP growth was in line with estimates at 2.3% quarter-over-quarter annualized, driven by a consumer spending increase of 4.2%

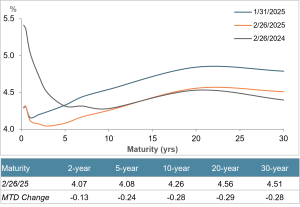

- Treasury rates fell across the curve this week, particularly in the long-end, which declined nearly 30bps on the week and hit year-to-date lows across tenors

- The investment-grade market capitalized on lower funding costs, issuing $51 billion this week versus expectations of $30 billion

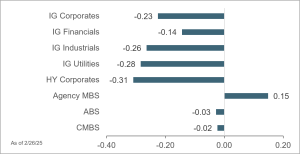

- Investment-grade corporate spreads widened by 6bps on the week to 83bps, as yields decreased by 19bps to 5.10%, the lowest since December after sixth consecutive days of declines

- The high-yield primary market had a quiet week with only $2 billion in new issues

- High-yield spreads widened this week by 12bps to 274bps as yields fell by 10bps to 7.13%, a 10-week low amid weak consumer confidence data and drop in new home sales

- Agency MBS spreads fell by 1bp to 32bps over the week as the 30-year mortgage rate dropped below 7% for the first time since early December

- Muni/Treasury ratios rose across the curve against a backdrop of healthy issuance, as the pace year-to-date exceeded 2024’s by 18%; municipal bond funds experienced inflows of $635 million

Treasury Yield Curve

Month-to-Date Excess Returns