Politics aside, investors on both sides of the aisle will likely agree that the first 100 days of President Trump’s second term were anything but predictable. But what about the next 100 days? Or the 1,200 days after that? While we expect the President to focus on Capitol Hill and his legislative agenda, when it comes to interest rates and election outcomes, IR+M is decidedly out of the forecasting business. Yet we are in the business of unearthing great bonds at great prices. And from our vantage point, we see opportunities for discerning, disciplined investors who can cut through the political noise and remain anchored in sound fundamentals.

- Bills, bills, bills. President Trump’s “One, Big, Beautiful” budget bill is taking center stage in the House as pundits question its impact on the deficit. House Speaker Mike Johnson intends to send the bill to the Senate by Memorial Day, and then to the President by July 4th. With the country’s August cash crunch looming, lawmakers may need to raise the debt ceiling by mid-July to avoid default.

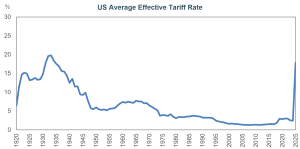

- Ever-lasting peace in Switzerland? The surprise 90-day détente in Switzerland between US and Chinese officials resulted in a dramatic rollback in tariffs. The US reduced tariffs on China from 145% to 30%, and China lowered tariffs on the US from 125% to 10%. Stocks soared on the news, rising more than 1,000 points on the day.

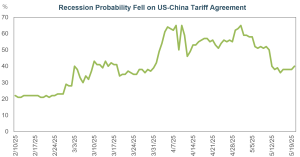

- Recession risk is declining. Prior to the tariff breakthrough with China, the odds of a recession reached as high as 65%. On the heels of the trade agreement, that estimate fell from 52% to 39% - the lowest level since Liberation Day on April 2nd.

- Higher education is on the hot seat. Some of the nation’s wealthiest universities are squarely in the Trump administration’s crosshairs as the White House turns up the heat financially. Harvard has captured headlines as it has rejected federal demands, and in return has had over $2 billion in grants and contracts frozen. House Republicans are now floating legislation that would create a tiered tax on college endowments of more than $500,000 per student, increasing the tax from 1.4% to as high as 21%.

- The future of tax-exemption could hang in the balance. President Trump has reiterated his intention to revoke Harvard’s tax-exempt status, a decision that ultimately resides with the IRS and would almost certainly trigger legal challenges. The move, which would be precedent setting, would almost certainly trigger lawsuits.

-

- The IR+M word. Universities are increasingly turning to the municipal bond market to bolster their balance sheets. Year-to-date through April, the higher education sector’s borrowing was up 20% y/y. Some investors are concerned that, in an effort to extend tax cuts, certain sectors – like higher education – may be prohibited from borrowing in the tax-exempt market. We believe this is unlikely.

- And then there were none. After a 2023 forewarning, Moody’s joined its two counterparts, S&P and Fitch, and lowered the US’ credit rating from Aaa to Aa1. Moody’s cited the US’ increased government debt and interest payment ratios as drivers of the move. For an encore, Moody’s then downgraded the ratings of five large US banks due to the removal of the US government support uplift, as well as several utilities and life insurers.

- From the IR+M desk. With President Trump’s first 100 days behind us, we turn our sights to the next 100 and beyond. Amid rising tariffs, market turbulence, and government restructuring, we have learned to expect the unexpected and question every assumption. While we do not foresee a return to February’s M&A exuberance, as spreads rebound, we are maintaining a cautious risk posture and selling into strength. Additionally, we are capitalizing on pockets of opportunity and buying some of our favorite bonds. We remain squarely focused on the potential for stagflation, a recession, and a higher-for-longer rate environment – unless an economic slowdown changes the equation. Through it all, prudent security selection remains our hallmark.