1Q25 Market Themes & Outlook

- Uncertainty permeated the market as tariff announcements dominated headlines and caused elevated volatility.

- Sentiment has softened as consumers and businesses expect higher inflation and slowing economic growth.

- Fundamentals remain healthy but may deteriorate if the economy becomes more pressured.

- The Fed must evaluate the potential impact of higher inflation, lower growth, and a rapidly changing political environment.

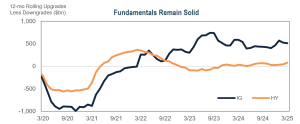

Taxable Sectors – Corporates

- Corporate fundamentals are healthy, but all eyes are on the trajectory of earnings and margins in anticipation of slower growth and higher tariffs – but are far from recessionary levels. We maintain a cautious risk posture and remain defensively positioned to deploy into pockets of spread widening and continue to see opportunity within corporates through thoughtful security selection.

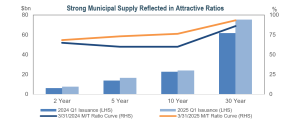

Tax-Exempt – Municipals: Ratios on the Rise

- Over the past year, Muni/Treasury ratios have risen across the curve due to the impact of increased supply and policy uncertainty as the question of whether tax-exemption will remain a feature of the municipal market pulls issuance forward. Current levels suggest value in municipals relative to corporates and reflect attractive entry points into the asset class.

Sources: Bloomberg as of 3/31/25, unless otherwise noted. Top left chart/table: Returns, yields, and spreads are from the respective Bloomberg indices as of 3/31/25. After-tax yields assume the highest federal marginal tax rate of 40.8%. Bottom left chart: Percentile calculated using monthly spread going back 20 years. Top right chart: IG = investment grade corporates and HY = high yield corporates based on the average rating across Moody’s, S&P, and Fitch. 12-month Rolling Upgrades Less Downgrades sourced from BofA Global Research as of 3/31/25 using monthly volumes and face amounts. The views contained in this report are those of IR+M and are based on information obtained by IR+M from sources that are believed to be reliable but IR+M makes no guarantee as to the accuracy or completeness of the underlying third-party data used to form IR+M’s views and opinions. This report is for informational purposes only and is not intended to provide specific advice, recommendations, or projected returns for any particular IR+M product. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission from IR+M. “Bloomberg®” and Bloomberg Indices are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the index (collectively, “Bloomberg”) and have been licensed for use for certain purposes by IR+M. Bloomberg is not affiliated with IR+M, and Bloomberg does not approve, endorse, review, or recommend the products described herein. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to any IR+M product.