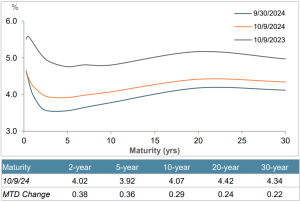

- Interest rates rose across the Treasury curve as investor expectations for the pace of rate cuts moderated amid mixed employment and inflation data

- Nonfarm payrolls came in at 254,000, above survey consensus estimates, and September's unemployment rate dropped to 4.1%; however, initial jobless claims were higher than expected at 258,000 versus 230,000

- The year-over-year change in CPI was 2.4% as of September, slightly higher than expected, but still the lowest figure since March 2021

- Core CPI, CPI minus food and energy, rose 3.3% on the year, higher than expectations of 3.2%

- Rate cut expectations for the rest of the year have dropped from 75bps worth of cuts to 50bps following the recent release of economic data

- Investment-grade issuance totaled $26 billion month-to-date, with dealers estimates calling for $95 billion in October; high-yield issuers have brought $8 billion of new debt so far this month

- Investment-grade yields rose by 23bps to 4.95% while spreads tightened by 7bps to 82bps on the month the tightest level since September 2021

- High-yield corporate spreads tightened by 5bps to 290bps on the month and yields rose by 24bps to 7.23%; CCC-rated corporates continued to outperform the broader high-yield market

- Agency MBS underperformed corporates month-to-date despite MBS spreads tightening by 2bps to 40bps; the 30-year fixed mortgage rate increased by 31bps to 6.96%

- Municipal bond mutual funds experienced the eighth straight week of inflows with nearly $1.5 billion added

- Municipals across the curve outperformed Treasuries as muni/Treasury ratios decreased month-to-date

Treasury Yield Curve

Month-to-Date Excess Returns