- Treasury bond yields continued to rise along the curve while Treasury bill yields fell slightly on the week as the market digested the latest economic data and potential implications of inflation under the new administration

- Changes in CPI and Core CPI, CPI less food and energy, were both in line with expectations, as CPI rose by 2.6% and Core CPI rose by 3.3% year-over-year in October

- The Producer Price Index (PPI) and Core PPI rose by 2.4% and 3.1%, respectively, both slightly higher than expected

- Initial jobless claims for the week reached the lowest level since May at 217,000, below expectations of 220,000, while continuing claims were in line with expectations

- Future markets are pricing in another 25bp cut at next month’s Federal Reserve meeting as economic data continues to show resiliency

- Investment-grade weekly issuance totaled nearly $44 billion, surpassing dealer expectations of $35 billion, as new deals continued to receive robust investor demand; high-yield issuers priced roughly $4 billion of new debt this month

- Investment-grade yields remained unchanged on the week, while spreads narrowed slightly by 1bp to 76bps

- High-yield spreads tightened by 10bps to 255bps and reached their tightest levels since 2007, while yields fell 8bps to 7.19%

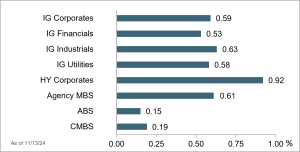

- Agency MBS outperformed other securitized sectors month-to-date; MBS spreads tightened nearly 3bps to 39bps as spreads continue to remain tight to the 5-year average of 45bps

- The 30-year fixed rate mortgage rate ticked up by 5bps to 7.29%, prompting homeowners to temper refinance expectations

- Munis outperformed Treasuries on the week as muni/Treasury ratios decreased across all maturities

- Municipal bond funds recorded $165 million of net inflows, marking the fourteenth week of positive inflows

Treasury Yield Curve

Month-to-Date Excess Returns