- Risk assets remained relatively stable as volatility decreased compared

to earlier in the month, while economic data continued to show a less

confident consumer- The S&P 500 rose on the week despite a dip on Wednesday,

as President Trump proceeded with a 25% tariff on automakers

and suggested new levies on Canada and the European Union - Consumer confidence, as measured by the Conference Board,

stood at 92.9 – its lowest point since early 2021 – amid

economic policy uncertainty and a rise in inflation expectations - Labor market data held steady as both initial jobless claims and

continuing claims came in slightly below expectations, at

224,000 and 1,856,000, respectively

- The S&P 500 rose on the week despite a dip on Wednesday,

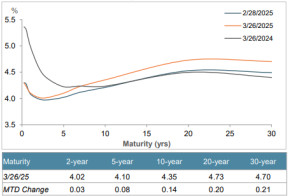

- The Treasury yield curve steepened, with the 30-year rate increasing

by 15bps week-over-week, while shorter tenors rose modestly - Both investment-grade and high-yield primary markets saw heightened

activity as issuers rushed to sell debt amid worries that a potential

slowdown in growth could reduce investor risk appetite- Investment-grade issuance totaled $41 billion, surpassing

expectations of $30 billion, and high-yield borrowers brought

roughly $5 billion of new deals to the market

- Investment-grade issuance totaled $41 billion, surpassing

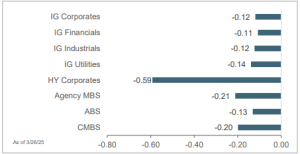

- Investment-grade spreads widened by 1bp week-over-week to 90bps,

with yields increasing by 9bps to 5.23%; high-yield spreads remained

unchanged at 314bps, and yields increased by 4bps to 7.57% - Agency mortgage-backed securities (MBS) underperformed other

securitized sectors, with spreads widening by 1bp to 36bps- Delinquencies rose among first-time homebuyers amid

declining housing affordability

- Delinquencies rose among first-time homebuyers amid

- Municipal bond funds recorded $19 million of inflows last week,

marking five consecutive weeks of positive flows; Muni/Treasury ratios

rose across the curve, except for the 30-year tenor

Treasury Yield Curve

Month-to-Date Excess Returns