- Markets digested a heavy slate of news developments this week, including an assassination attempt on former President Trump, weakness in technology equity shares, and dovish comments from Fed officials

- US retail sales beat estimates during June, as consumers directed spending toward categories where prices have fallen

- The Producer Price Index (PPI) rose 2.6% year-over-year, slightly above estimates; however, the PPI components that contribute to Core PCE were significantly lower than expected

- Several Federal Reserve (Fed) officials spoke this week, highlighting improved data on inflation and signaling rate cuts may be around the corner, which sent Treasury yields tumbling across the curve

- The 2-year yield fell 18bps to 4.44% and the 30-year yield dropped 10bps to 4.38%

- Investment-grade issuers priced $38 billion this week, above estimates, with large domestic banks leading the majority of issuance

- Corporate spreads widened by 1bp week-over-week to 91bps, and yields dropped 13bps to 5.21%

- High-yield bonds recorded their longest gaining streak since 2020 of 11-straight days; meanwhile, primary market activity was light, with only $1 billion of supply

- Spreads tightened by 3bps to close at 304bps, and yields fell 19bps lower to 7.61%, the lowest level since last December

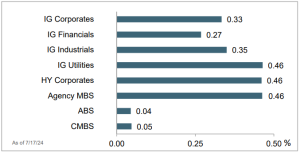

- Following the largest month of supply since 2006, the continued issuance of asset-backed securities (ABS) led ABS to underperform other securitized products

- Year-to-date municipal issuance totaled $246 billion, over 36% higher than this time last year, as states and municipalities seek funding to finance new infrastructure projects and have issued tax-exempt debt to refinance Build America Bonds

Treasury Yield Curve

Month-to-Date Excess Returns