- The market reacted positively to President-elect Trump’s selection of Paul Atkins as the next chairman of the Securities and Exchange Commission and to Federal Reserve (Fed) Chair Powell’s positive commentary on the state of the US economy despite mixed economic data

- October’s job openings (JOLTS) report surprised to the upside as 7.74 million openings were reported versus forecasts of 7.52 million

- ADP private employment rose by 146,000 jobs in November versus expectations of 150,000 jobs; notably October’s figure of 233,000 received a substantial downward revision to 184,000

- ISM Manufacturing PMI increased to 48.4 in November, exceeding expectations of 47.5, driven by a surge in new orders

- Investment-grade issuers priced over $23 billion of fresh debt month-to-date, slightly below dealer expectations of $25 billion; dealer estimates are calling for $40 billion of new issues for December

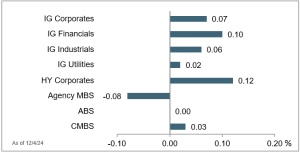

- Yields in the investment-grade corporate market fell by 4bps to 5.01%, while spreads tightened by 1bp to 77bps

- In the high-yield market, issuers priced just over $2 billion in new bonds month-to-date and CCC yields fell to a 31-month low of 9.64%, fueling the recent rally

- High-yield spreads tightened by 4bps to 262bps, while all-in yields decreased by 7bps to 7.07%, a two-month low

- Agency mortgage-backed securities (MBS) have underperformed other securitized sectors on the month as spreads widened by 1bp month-to-date to 42bps, however, spreads remain tight relative to the 5-year average of 45bps; the 30-year mortgage rate remains elevated at 7.03%

- Municipal bond funds recorded $625 million of inflows, marking the seventeenth consecutive week of asset increases as munis outperformed Treasuries month-to-date

Treasury Yield Curve

Month-to-Date Excess Returns