- As was widely expected, the Federal Reserve (Fed) cut rates by 25bps at Wednesday’s FOMC meeting, bringing the fed funds target range to 4.25% - 4.50%

- The updated FOMC dot plot showed that officials expect a more gradual pace of future rate cuts, with only two quarter-percentage cuts penciled in for the upcoming year

- Equity prices and Treasury yields sold off in response to the Fed’s hawkish tone and outlook of persistent inflationary pressures next year

- The S&P 500 posted a loss of 2.9% on Wednesday – the worst single day of performance since August

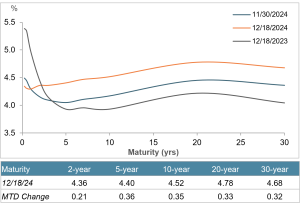

- The 10-year Treasury yield climbed by 12bps day-over-day to 4.52%, the highest point since May of this year

- There was no new issuance in the investment-grade corporate market this week, and expectations are for little to no additional primary market activity until 2025

- $1.5 trillion in new investment-grade corporate bonds priced in 2024, a 26% increase from 2023

- Corporate spreads widened by 2bps week-over-week to 76bps, and yields rose by 23bps to 5.29%

- High-yield spreads widened by 8bps to 267bps, and yields rose by 27bps to 7.35% – the highest level since August

- Year-to-date high-yield corporate supply has totaled $279 billion, 59% higher than last year’s pace

- Agency mortgage-backed securities (MBS) underperformed other securitized sectors amid the uptick in rate volatility; spreads widened by 6bps to 46bps and mortgage rates increased by 18bps to 7.19%

- Investors added another $1 billion into municipal mutual funds, marking the 19th straight week of net inflows since August, and bringing the cumulative total to $19 billion

Treasury Yield Curve

Month-to-Date Excess Returns