Let’s hop into our time machines for a moment. We’ll take a 9-month jaunt back to the end of January. Now we’re sitting shoulder-to-shoulder in a crowded restaurant. A college basketball game plays on television – the arena packed with bobbing student fans. An adjacent table hums with chatter of a Caribbean vacation in March. Someone asks, “What is the novel coronavirus?” A Wall Street analyst declares, “The consensus on the economy anticipates a calm and uneventful year ahead.” The 10-year Treasury closes at 1.52%.

We can’t help but project the present into the future. When markets are calm, we expect them to stay calm. When markets unhinge, we fear they’ll remain unhinged. As Benjamin Graham put it, “In the financial markets, hindsight is forever 20/20, but foresight is legally blind.” Daily price action lulls us into a sense of complacency, then plays nasty tricks on us. But markets also reward patience. In the meantime, the 2020 rollercoaster continues. What’s an investor to do?

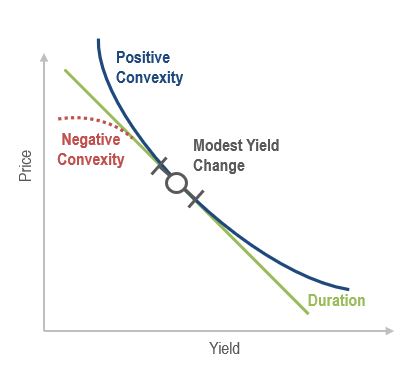

The Power of Convexity

Buy insurance. Fixed income provides a subtle but prescient policy termed convexity. Convexity is why the dollar price of a bond will not fall to zero even if rates climb into the stratosphere. Convexity is what limits duration risk even if a bond’s cashflows extend beyond our lifetimes (e.g., hundred-year maturities). Convexity is the mathematical essence of compound interest – Einstein’s 8th wonder of the world. It can be a nice treat for savvy bond investors.

Positive convexity is embedded in bonds with fixed cashflows. Duration and convexity metrics constitute a second-order approximation of a bond’s price sensitivity to changes in yield. Duration is typically dominant, but without convexity’s curvature, the relationship would be too linear (e.g., a large rate jump would result in negative bond prices).[1]

Currently, a 10-year par bond’s convexity is close to one, while a 30-year par bond’s is greater than six. However, credit spreads are an important ingredient. While corporate bonds can have the same convexity as comparable duration Treasuries, credit spread movements impact the conversion of that convexity into price performance. If spreads are widening into a rate rally (risk-off) or tightening into a rate sell-off (risk on), the realized convexity returns may be lower. This trick has been played on investors in the past, and can be more potent in a low yield environment.

Negative (Spooky) Convexity

Then there are embedded bond options. When a bond’s cashflow timing varies, “unconventional” convexity can have an outsized impact on returns. If an issuer or borrower holds the option – as with an early redemption call, mortgage-backed prepayment, or optional maturity extension – the convexity is likely negative. The magnitude of such is contingent on the bond’s yield volatility, time to redemption/extension, and price difference with par (or equivalent). The latter is key — a bond price significantly “in-the-money” or “out-of-the-money” will have less negative convexity. Take mortgage-backed securities (MBS), for example. Mortgage borrowers typically have continuous options to refinance. While their behavior is not always rational, statistical trends in their willingness and ability to refinance can be uncovered. When MBS is highly refinance-able (such as now), convexity and duration become inexorably intertwined. Small interest rate moves may trigger large duration shifts if borrowers are “on-the-fence” about refinancing. But the investor must be careful not to embed interest rate forecasts into MBS analytics.

Case-in-point: the winter of 2019. An investor might have been tempted to set MBS durations that implied refinancing activity was more likely to slow than quicken over the next twelve months (based on Wall Street forecasts). But this would have been a misguided view on the eve of the sharp rate rally in the spring of 2020. The investor would have suffered a major convexity hit in the portfolio’s MBS holdings. With enough allocation, this convexity event could rival the performance drag of an explicit duration bet at the portfolio level. So be careful, lest a small convexity trick grows into a large one via MBS duration management.

Positive Convexity (A Tasty Treat!)

On the other hand, underpriced positive convexity is one of the most powerful concepts in finance. It can provide a positive pay-off without requiring investors to correctly predict the future of interest rates. Take 2020, for example. The rate rally in March could have generated significant positive convexity returns at the portfolio level all else equal. But that caveat brings us to our final point: DON’T MAKE DURATION BETS! Duration’s impact on price often swamps that of convexity. To benefit from positive convexity, the bond manager should remain duration neutral. Otherwise, it’s like forgoing the opportunity to shave the dice at the craps table only to go to the roulette table and bet it all on black. Don’t ruin your convexity treat!

It was only a year ago that bond investors could earn more yield in a money market account than they can with today’s Bloomberg Barclays Aggregate Index (and its more than 6-year duration). While duration risk remains double-edged, convexity is guaranteed to be one-sided. Yet rating agencies are silent on convexity risk. Thus, managers must not be fooled by bonds that derive attractive yields from embedded issuer/borrower options. To that, we quote Richard Feynman: “…and the easiest person to fool is yourself.”

[1] Convexity is the derivative of duration; as a result, it also tells us the rate of duration change along the yield curve.