- Once a feature largely confined to the High Yield corporate bond market, bonds issued below par are becoming more common within the investment grade Asset-Backed Securities (ABS) market

- Bond buyers need to examine the risks before investing, given that extension – rather than impairment – is the more relevant risk for senior ABS bondholders. Moreover, the investment grade ratings that ABS carry do not reflect this risk

Who doesn’t like a discount? Black Friday, Cyber Monday, and Amazon Prime Day are practically holidays in the United States, with bargain hunters sometimes waiting for hours to be first in line to secure a good deal.

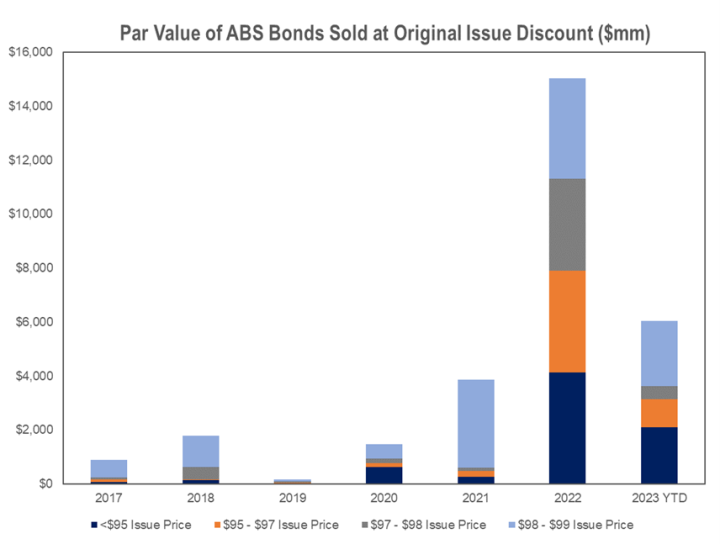

Recently, the discounting trend seems to have taken hold within the investment grade ABS market. While the dynamics within the ABS market are not quite the same as the retail market, the overall trend is: more and more deals are being issued at steep discounts to par.

The reason behind this trend, of course, lies with interest rates. Facing rapidly increasing costs of debt, many ABS issuers have opted to complete transactions with below-market coupons (4-6%), giving investors the rare opportunity to buy bonds at significant discounts to par. Meanwhile, the stated yields of these discount bonds are exceedingly high, in some cases surpassing 7%.

Given that Original Issue Discounts (“OIDs”) are a relatively new phenomenon to the ABS market, it seems important to ask: are these OIDs a sign of attractive value, or are they instead a “value trap”? Before we answer this question, it is worth exploring how OIDs have traditionally been used in other bond markets.

Exhibit 1: Par Value of ABS Bonds Sold at An Original Issue Discount

Background: Original Issue Discounts (OID) in High Yield

Before the recent increase in interest rates, OID issuance was largely confined to lower-rated, higher risk markets such as the High Yield and Leveraged Loan markets. Issuers in these markets have used OIDs as a means of enticing yield hungry investors who may have otherwise shied away from purchasing the company’s debt.

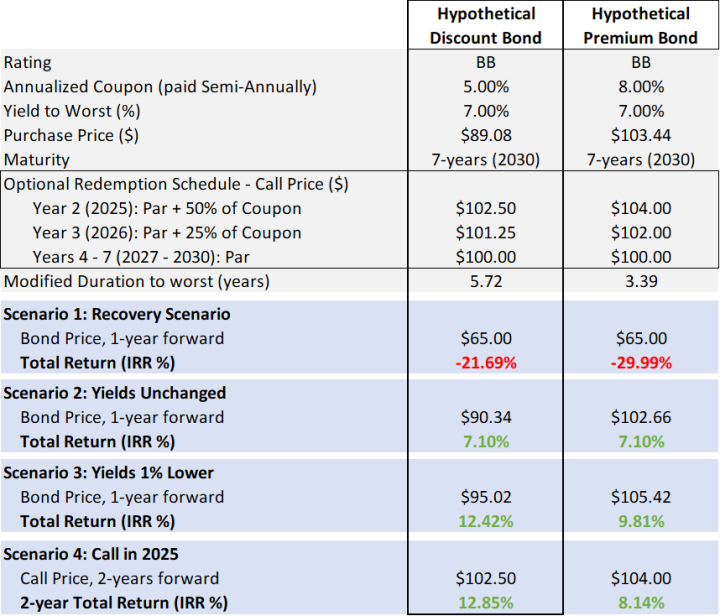

Indeed, the usage of OIDs within those markets has been largely driven by investor, rather than issuer, preference. By investing in this relatively risky debt at a lower price point, investors in these markets effectively lower their overall risk of principal loss, reducing downside risk. At the same time, in what is typically a call-constrained asset class, OID buyers more heavily participate in upside scenarios as well. As shown in Exhibit 2 below, lower priced bonds outperform higher priced bonds in “recovery,” declining yield, and “call” scenarios.

Exhibit 2: Discount Bonds in the High Yield Market Typically Outperform Higher Priced Bonds With Identical Yields

OIDs Within the ABS Market: A New Phenomenon Driven by Higher Interest Rates

While OIDs have become commonplace within the High Yield and Leverage Loan markets, they are still relatively new within the investment grade ABS market. And unlike the corporate bond market, much of this OID issuance has been driven by issuer, rather than investor, preference.

Higher interest rates have started to put pressure on the all-important Debt Service Coverage Ratio (“DSCR”), a ratio that measures asset cash flow relative to debt servicing costs. For some issuers, the severe reduction in the DSCR has practically made OID issuance a necessity, with many issuers coming dangerously close to breaching minimum DSCR compliance thresholds.

OIDs Within the ABS Market: Not the Bargain Many Hoped For

How should ABS investors feel about the increasing prevalence of bonds being issued with large OIDs? Unfortunately, the “discount” they think they are getting could instead be a value trap. Besides the fact that OID issuance is a clear sign of a deficiency in asset cash flow, the ABS bonds that are being issued at discounts have worse return profiles than higher coupon bonds in certain extension scenarios.

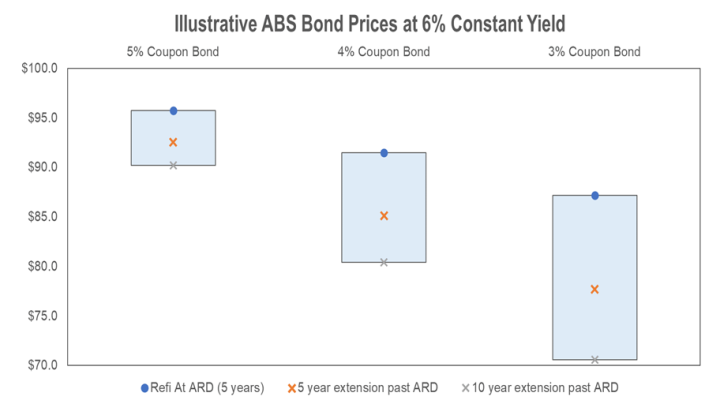

As shown in Exhibit 3 below, lower coupon bonds experience much steeper price declines in various extension scenarios where the debt remains outstanding beyond the Anticipated Repayment Date (“ARD”). The longer it takes to repay the principal balance, the larger the drop in bond price. Adding insult to injury, holders of the lowest coupons experience the largest declines in bond value. Unfortunately, this risk of extending beyond the ARD is not apparent from the investment grade ratings that many ABS bonds carry, given that rating agencies use the Legal Final Payment Date – rather than the ARD – as the guidepost for determining the likelihood of full principal repayment (and thus ratings). As we discussed in a prior blog post, the Legal Final Payment Date for deals backed by long-dated assets can be in excess 15 years beyond the ARD.

Exhibit 3: Unlike Discount Bonds in the High Yield Market, Discount ABS Underperform Higher Priced Bonds in Many Downside Scenarios

Reliance Upon Lower Interest Rates at ARD Deserves Scrutiny

Before investing in deals with large OIDs, ABS investors need to examine the issuer’s ability to repay investors back at par at the ARD. The most simple and straightforward ways to repay the discount are through scheduled amortization and/or asset value growth, both of which effectively “de-lever” the deal. If either of these de-levering features is not present, investors are essentially making a gamble that market yields will be lower at the ARD, allowing issuers to refinance OID bonds with new bonds priced at par. Given the unpredictable nature of interest rates, however, investors should heed caution – especially since securitization sponsors have no obligation to plug the discount “hole” with their own equity. Ultimately, the “discount” that many ABS bondholders are hoping for could turn out to be one long, extended disappointment.