If you’ve ever seen a James Bond movie, you’re probably familiar with the basic plot line. James Bond (or “007” as he’s commonly called) gets caught up in some clandestine mission to save the world, performs impossible stunts like jumping out of a plane without a parachute, and inevitably prevails as a hero.

At this juncture in the bond market, many Commercial ABS issuers seem to have found themselves in the plot of a James Bond thriller. Commercial ABS bond yields have more than doubled over the last year as the Federal Reserve (Fed) battles inflation, creating refinancing risk for issuers with balloon-style repayment structures. Thanks to a very manageable near-term debt maturity schedule, however, many Commercial ABS issuers just might live to “Die Another Day.”

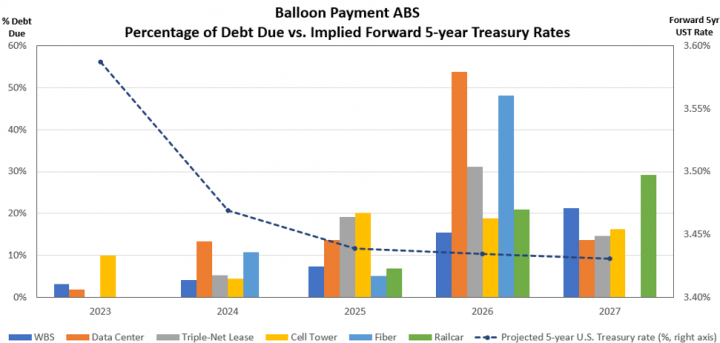

As you can see in Chart 1 below, most Commercial ABS sectors with balloon-style repayments have modest Anticipated Repayment Dates (“ARDs”) in 2023 and 2024. At the sector level, near-term debt maturities are low, with no more than 15% of total debt coming due in the next two years.

Chart 1: Balloon Payment ABS Debt Maturity Schedule & Forward Rates

Source: Bloomberg as of 2/9/23. Debt schedule reflects current bond balances, not projected bond balances at the relevant Anticipated Repayment Date (“ARD”). Debt schedule does not incorporate revolving facilities.

But what if inflation proves to be long-lasting, and benchmark rates remain stubbornly high through 2025/2026? That’s when things could get interesting. Currently, the market is pricing in forward 5-year U.S. Treasury rates in the mid 3% range, which could easily translate into 5 – 6% weighted average bond yields for senior and subordinated ABS debt down the road. Interest rates this high can quickly erode the Debt Service Coverage Ratio (“DSCR”), a metric commonly used to assess the health of an ABS deal. This metric measures the amount of cash flow generated by the asset pool relative to debt service costs, and typically needs to exceed a minimum threshold to enable refinancing debt to be issued to pay off the outstanding bonds.

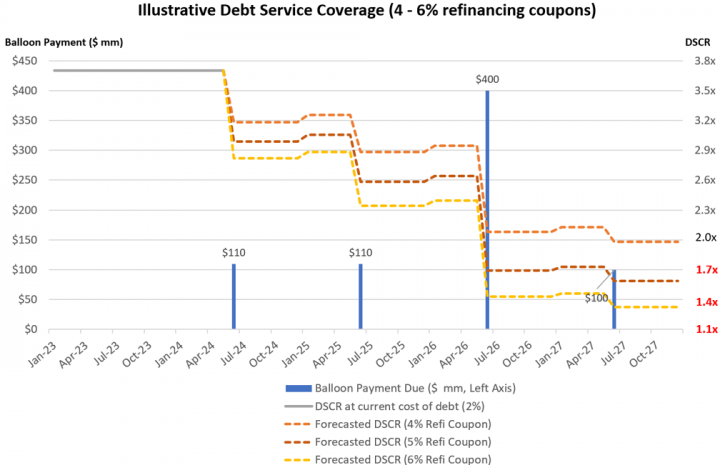

As shown in the chart below, gradually increasing a highly levered issuer’s weighted average cost of debt from 2% to 4% over a 5-year period can potentially cause the DSCR to roughly be cut in half, from 3.7x to just 2.0x. Increasing the cost of debt further to the 5 – 6% range pushes the projected DSCR below 2.0x, a threshold commonly structured as the minimum level needed to issue refinancing debt. This of course assumes that revenues only increase at a compounded annual rate of about 2%, which is common for many sectors with long-dated leases such as Data Center, Cell Tower, and Triple Net lease ABS. Contracted revenue streams for other sectors such as Franchise Whole Business Securitizations (“WBS”) and Railcar Leasing ABS tend to be much shorter in nature, potentially allowing for revenues to reset higher with inflation/rates.

Chart 2: Illustrative Debt Service Coverage Ratios (4 – 6% refinancing coupons)

Source: IR+M Analytics. Assumes a 2% annual rent escalator and a 1% annual servicing fee (as a percentage of the debt balance)

So what does this mean for Commercial ABS bonds with elevated refinancing risk? First, it’s worth clarifying that ARDs are just that – Anticipated Repayment Dates. The actual Legal Final Payment Date – or date by which the debt must be paid off to avoid a default – can be in excess of 15 years beyond the ARD. An issuer can therefore fail to repay a bond by the ARD without triggering a default, causing the debt to remain outstanding until sufficient residual cash flow that otherwise would have flowed to equity is used to pay down the debt balance. Depending on how long it takes for the deal to sufficiently de-lever such that the LTV and DSCR are back in compliance, the bond duration can extend by a meaningful amount – having large implications for pricing and spreads.

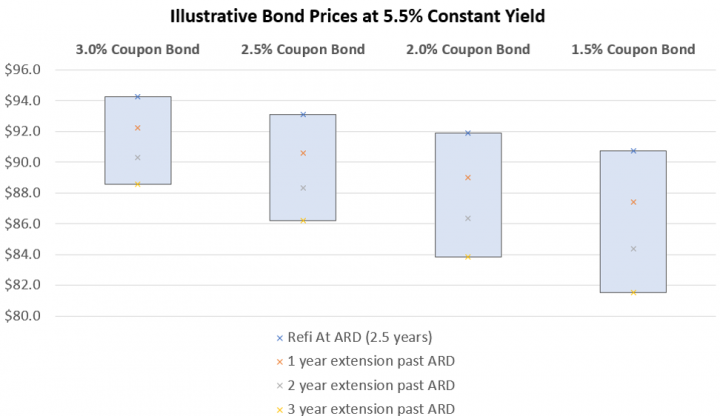

Chart 3 below provides an illustrative example of how the extension of a security’s repayment date can impact the price of a bond. Assuming a constant yield of 5.5%, a 3% coupon bond with a 2.5-year ARD would suffer a 2.1 point drop in price when the repayment date extends by 1 year. As the length of bond extension gets longer, however, so does the severity of the drop in price. The same 3% coupon bond suffers a 5.7 point drop in price when the repayment date extends 3 years beyond the ARD, from $94.3 to $88.6. This impact of bond extension is particularly acute for low-coupon bonds, whose returns are heavily dependent on the repayment of principal. As shown in the example below, extending a 1.5% coupon bond by 3 years results in a whopping 9.2 point price drop, assuming a constant 5.5% yield.

Chart 3: Illustrative Bond Prices at 5.5% Constant Yield

Source: IR+M Analytics. Above bond prices do not incorporate the receipt of the minimum [5]% Post-ARD step-up interest, which is both unrated and subordinated in the waterfall to senior and subordinated bond principal. Bond prices also assume 2% bond amortization (paid monthly) from the ARD date to the ultimate refinancing date

Where will bond yields end up in 2025/2026? Like many bond market participants, I’m anxiously waiting to see how this movie plays out. Will the Fed save the day by gradually lowering interest rates, or will rates stay higher for longer? In the meantime, we should expect issuers to address DSCR deterioration by pricing new debt at below-market coupons and potentially reducing leverage on newly funded assets. If DSCR deterioration starts to inhibit the ability to refinance, issuers could sell assets to pay off debt or even use cash raised by the securitization sponsor to repay the bonds. Given the non-recourse nature of securitization financing, however, bondholders should not rely on the sponsor bailing out the ABS bondholders– indeed, it is usually bondholders that are left “holding the bag”. Recent precedent transactions indicate that issuers are inclined to ask bondholders to temporarily waive the Rapid Amortization Event that would go into effect after the ARD in exchange for a minimal one-time fee. Many bondholders would argue that this tactic does not properly compensate them for the post ARD step-up interest that would otherwise accrue (typically a minimum of 5% per year). For now, however, DSCRs are in compliance and any discussion of bond amendments is purely hypothetical. So grab your popcorn and get ready to see if issuers can make a James-Bond like escape.