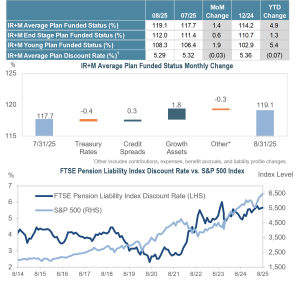

IR+M Funded Status Monitor

- Our sample Average Plan funded status increased by 1.4% to 119.1% in August, driven primarily by positive returns in growth assets.

- Discount rates¹ decreased by 0.03% in August, from 5.32% to 5.29%.

- Risk assets rallied amid mixed labor market and inflation data, with the S&P 500 rising 2.0% for the month. Fed Chair Jerome Powell signaled the Fed’s receptivity to a September rate cut, and the Treasury curve steepened as a result.

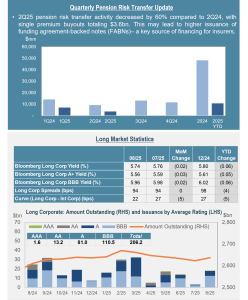

- Despite tightening to 89bps on August 15 – the narrowest level since May 1998 – long corporate spreads ended the month unchanged at 94 bps. Long-end issuance totaled $18 billion during the month.

¹The single effective discount rate shown is for the IR+M Sample Average Plan, calculated from the FTSE Pension Discount Curve. Pension Risk Transfer data sourced from LIMRA. Long issuance sourced from Bloomberg. Long issuance figures exclude 10-year bonds. The table in the long issuance chart shows the 12-month running total investment grade issuance by rating, through 8/31/25 in USD billions. Totals may not sum due to rounding.

Sources: Moody’s PFaroe, FTSE Russell (formerly Citigroup), LIMRA and Bloomberg. All data in the above commentary is as of 8/31/2025. Yields are represented as of the aforementioned date and are subject to change. The views contained in this report are those of Income Research + Management (“IR+M”) and are based on information obtained by IR+M from sources that are believed to be reliable but IR+M makes no guarantee as to the accuracy or completeness of the underlying third-party data used to form IR+M’s views and opinions. This report is for informational purposes only and is not intended to provide specific advice, recommendations, or projected returns for any particular IR+M product. Investing in securities involves risk of loss that clients should be prepared to bear. More specifically, investing in the bond market is subject to certain risks including but not limited to market, interest rate, credit, call or prepayment, extension, issuer, and inflation risk. “Bloomberg®” and Bloomberg Indices are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the index (collectively, “Bloomberg”) and have been licensed for use for certain purposes by IR+M. Bloomberg is not affiliated with IR+M, and Bloomberg does not approve, endorse, review, or recommend the products described herein. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to any IR+M product. Moody’s Analytics PFaroe® product used by IR+M includes market data and other information sourced from third parties under license. Certain licensors require Moody’s Analytics to make disclosures to, or to obtain acknowledgements or agreements from, IR+M and parties receiving the information from IR+M, which is effected by the disclosures and disclaimers available at https://static.pfaroe.com/DisclosuresAndDisclaimers/index.html. This material may not be reproduced in any form or referred to in any other publication without express written permission from IR+M.

IR+M Funded Status Monitor Assumptions:

Detailed methodology and assumptions for the IR+M Funded Status Monitor can be found at:

https://www.incomeresearch.com/wp-content/uploads/IRM-Funded-Status-Monitor-Whitepaper-2025.pdf