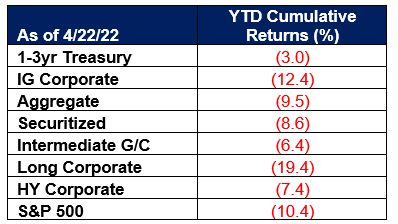

YTD Bond Returns Have Been Among the Worst Ever

Bonds of all types have had significant drawdowns this year as fears of inflation and Fed tightening are front and center in bond investors’ minds. Treasuries, Corporates, Securitized, Short, Intermediate, Long, Investment Grade, High Yield – it doesn’t matter – results have been among the worst periods we have ever seen. Even Short Treasuries, measured by the Bloomberg 1-3 Year Treasury Index, which have a pretty good track record of protecting capital over rolling 3-month periods, have experienced a 3.0% drawdown – their worst since the data started being tracked 30 years ago. The Bloomberg Aggregate Index (Agg) is down 9.5%, Long Corporates are down roughly 19.4%, and High Yield is down 7.4%. Surprisingly, equities have been relatively resilient, returning -10.4% YTD for the S&P 500.

What Now?

The move has been both significant and swift, precipitated more by fear and uncertainty than fundamentals. Of course, the deplorable war in Ukraine continues, though normally this type of event precipitates a flight to quality, so perhaps it is keeping a ceiling on how high Treasury rates can go. Inflation is rampant, at a 40-year high, and the Fed is moving quickly. Despite these overhangs, the US economy is still expected to grow by 2-3% this year, and corporate earnings by about 10%. Sanctions on Russia will reduce world GDP, but clearly have pushed inflation well beyond transitory. The consumer is flush with post-pandemic cash, supporting consumption, and employment is strong, increasing wage pressures. There is significant pent-up demand for travel, concerts, sporting events, etc. Manufacturing PMI has rolled over, but is still strong. The brief 2-year/10-year Treasury yield curve inversion is an oft-cited indicator of recessions, but the timing typically varies. It remains to be seen if the Fed’s vigilance will go too far and move the economy in that direction, or perhaps negotiate a soft landing.

Is It Time Yet?

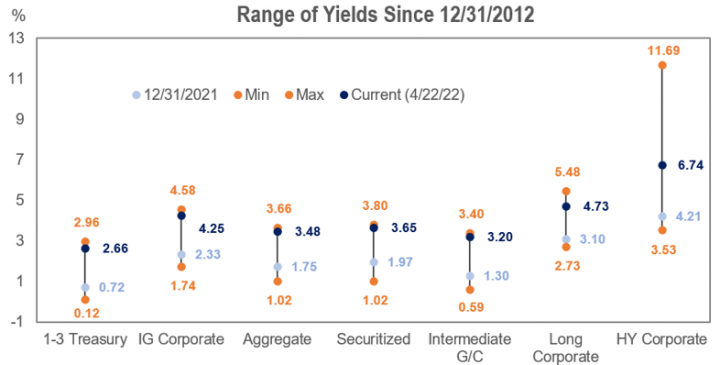

What is a bond investor to do? It may be time to nibble at the much higher rates available on short-term products – while 2-year Treasuries are up 194bps this year to 2.67%, 1-3 year Corporates are up 231bps to 3.43%. Other sectors of the market have seen similar increases in yields. The yield on the Agg is 172bps higher to 3.48%, while Long Corporates are 163bps higher to 4.73%. With the relatively limited recent drawdown in equities, the huge runup in recent years, and the rise in discount rates, we expect that improved funded status will cause many pension plans to rebalance in favor of bonds. Likewise, rates have moved higher in the US relative to many foreign markets, and though the move in the dollar has increased hedging costs, our bonds are still attractive to foreign buyers, supporting demand. Buyers will begin to emerge at more attractive rates.

This Too Shall Pass

Markets are resilient. Many periods of significant drawdown create attractive buying opportunities. There is often an overshoot, and prices can recover quickly. We are not predicting what rates will do, nor how Ukraine, inflation, or recession will play out, but it seems like the market has digested and discounted a fair amount of the potential economic fallout. For investors looking to add some yield to their portfolios at much better levels than anytime over the past 3+ years, it may make sense to begin to average in.

At IR+M, we manage a variety of strategies across the maturity and ratings spectrum, and would love to talk with you about your investing objectives and how we can help meet your needs. To view previous market commentary, please visit the What We Think section of our website.