4Q25 Market Themes + Outlook

- The economy is likely to benefit from both fiscal stimulus and monetary easing, with effects expected to be broadly felt.

- Within the FOMC, views remain divided, with a widening split reinforcing policy uncertainty.

- Higher-income households have benefited disproportionately from asset price gains relative to lower-income consumers.

- Capital spending and business investment are increasingly concentrated in AI and data centers, which are also expected to drive earnings growth.

Taxable Market Insights

- Corporate bond demand remains strong amid healthy fundamentals, elevated yields, and strong interest from annuities, retail investors, pensions, and overseas buyers.

- Investment-grade and high-yield issuance is expected to be heavy in 2026, driven by sustained tech investment, renewed M&A, balance-sheet re-leveraging, and large refinancing needs.

Tax-Exempt Market Insights

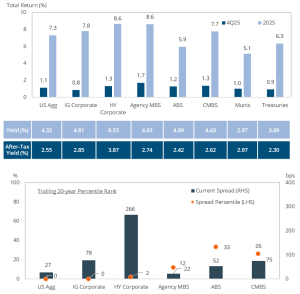

- 2025 marked a shift away from a risk-on market, with BBBs modestly underperforming higher-quality credits; high-quality carry led performance, particularly in housing and gas prepays.

- For 2026, general obligation bonds remain tightly valued, but spread opportunities persist in select revenue sectors, including airports, housing, gas prepays, and hospitals.

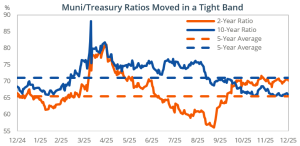

- Federal policy risk has eased with preservation of the tax exemption, though elevated issuance could limit further ratio tightening in 2026.

Sources: Bloomberg as of 12/31/25, unless otherwise noted. Top left chart/table: Returns, yields, and spreads are from the respective Bloomberg indices as of 12/31/25. After-tax yields assume the highest federal marginal tax rate of 40.8%. Bottom left chart: Percentile calculated using monthly spread going back 20 years. The views contained in this report are those of IR+M and are based on information obtained by IR+M from sources that are believed to be reliable but IR+M makes no guarantee as to the accuracy or completeness of the underlying third-party data used to form IR+M’s views and opinions. This report is for informational purposes only and is not intended to provide specific advice, recommendations, or projected returns for any particular IR+M product. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission from IR+M. “Bloomberg®” and Bloomberg Indices are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the index (collectively, “Bloomberg”) and have been licensed for use for certain purposes by IR+M. Bloomberg is not affiliated with IR+M, and Bloomberg does not approve, endorse, review, or recommend the products described herein. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to any IR+M product.