1Q26 Market Themes + Outlook

- Investors have been forced to navigate AI fears, private credit concerns, and the ongoing US-Iran conflict in 1Q.

- Resulting volatility was felt more in interest rates, which have moved higher, than in spreads.

- The labor market has been firm, and inflation has been well-anchored, although oil prices have risen meaningfully.

- FOMC projections imply one rate cut in 2026, however, the market has lost some confidence that the Fed will ease this year.

Taxable Market Insights

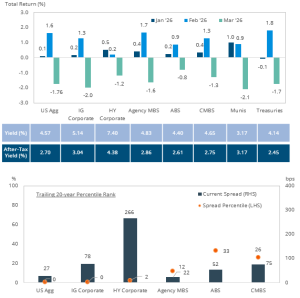

- Investment-grade credit saw rising dispersion amid macro uncertainty – energy issuers benefited from surging oil prices and software/AI lagged on obsolescence concerns. Despite volatility, record first quarter issuance and strong inflows supported demand, with spreads ending modestly wider (+10bps to 61bps).

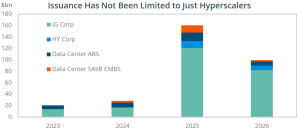

- Securitized assets outperformed Corporates and Treasuries, benefiting from relative insulation to macro risks; while agency MBS lagged on rate volatility, ABS issuance was robust, with continued growth in non-traditional sectors like data centers and infrastructure-backed deals.

Tax-Exempt Market Insights

- Municipal valuations improved in 1Q, with March’s sell‑off pushing yields higher and creating attractive entry points versus Treasuries and Corporates, particularly in longer‑duration, high‑quality tax‑exempt bonds.

- Heavy issuance and volatility widened spreads, creating selective opportunities in sectors such as Gas Prepay, Health Care, Housing, and certain GO bonds, where fundamentals remained sound.