The global spread of the coronavirus created economic uncertainty and extreme market weakness. Within the US Investment Grade bond market, the most significant spread widening in over ten years was driven mostly by market technicals as liquidity evaporated – in a scramble for cash, investors sold what they could.

We believe that the market has since somewhat normalized as government programs have helped support liquidity with direct purchases and numerous backstop facilities. Spreads have tightened and we feel investors can now focus on the fundamental picture, sorting through each industry to determine which may persevere, which may struggle to revert to normal, and which may have longer-term issues. Below, our Analysts have provided some color on the risks and opportunities across sectors, and the potential for fundamental industry changes going forward.

Checking the Rearview Mirror

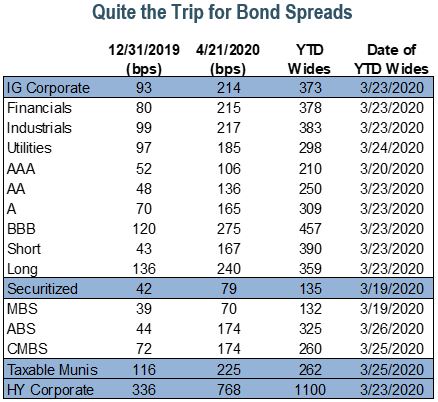

- Spreads entered the year near all-time lows, then widened as investors rushed to raise funds and liquidity was challenged. Since the Federal Reserve intervened, spreads have become more differentiated across sectors and credit quality.

- As fundamentals deteriorated, analysts were challenged to update models and reduce earnings estimates given the difficulty in predicting the scale and duration of the impact.

- Over $90 billion of debt was downgraded to below investment grade in March, and could potentially top $500 billion by year-end, which would increase the high yield universe by 25-50%.

- While funds from the largest stimulus bill in history are beginning to reach those in need, the speed and shape of recovery will be driven by the virus timeline and reopening the economy, not the stimulus.

- As we assess the uncertainty surrounding business disruption and unemployment, we expect some industries to be impacted more than others; recovery will not be uniform. Differentiating between industries and specific companies that can adapt and recover over the medium-term, and those that may suffer longer-term damage, can be the key to successful investing going forward. We believe active management and security selection will be crucial to navigating this environment.

Avoiding the Potholes

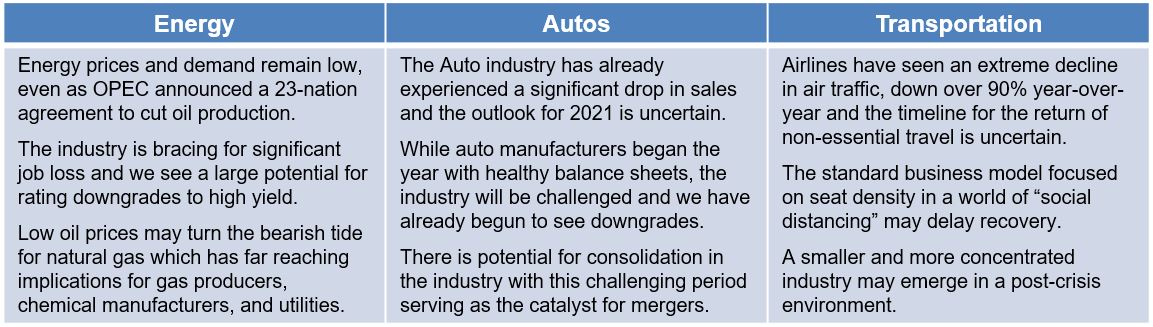

- The impact on the consumer weighs heavily on many industries, such as Energy, Autos, and Transportation.

- The downstream impact of unemployment trends has a long timeline. As a result, we are cautious in our investments and rely on our bottom-up analysis to evaluate risk and potential opportunities.

Some Bumps In the Road

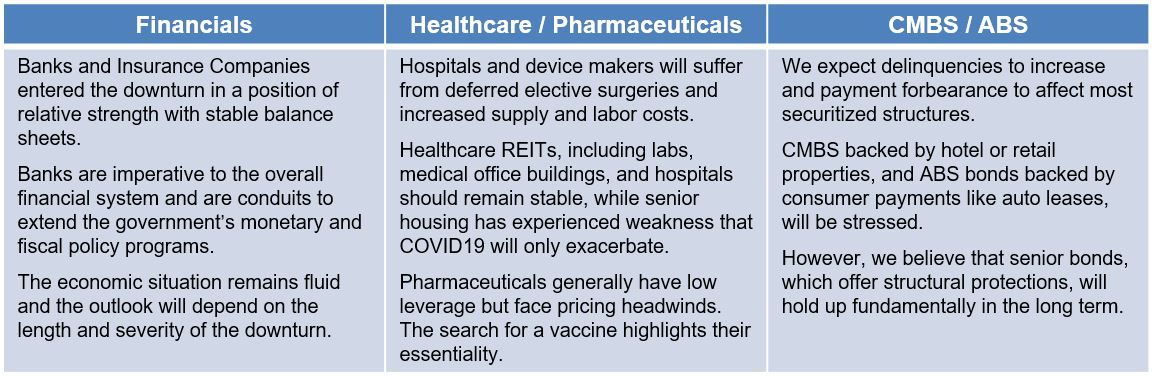

- Industries like Financials, Healthcare, and Pharmaceuticals have not escaped the impact of the economic downturn, and we feel confident that they are well-positioned to withstand the bumps in the road.

- CMBS and ABS have excellent structural protections, but issuance will be lower and methods of financing may change. Work-from-home may impact office demand longer term.

Open Road Ahead

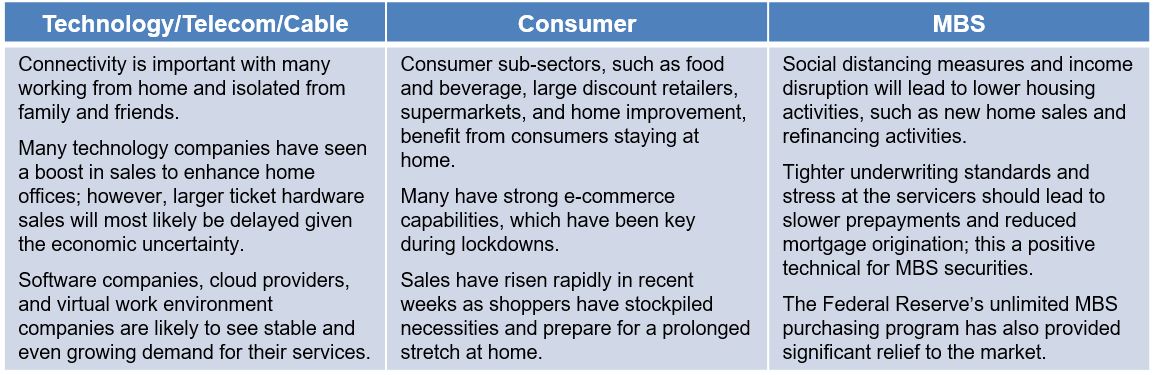

- Technology/Telecom/Cable and some Consumer sub-sectors have been less negatively impacted by the current lockdown, and have a more favorable degree of balance sheet flexibility.

- Agency MBS are implicitly backed by the Government, are supported by the Federal Reserve purchases, and provide important structural protections against forbearance, since the Agencies pay principal and interest on a timely basis.

Today’s extraordinary health crisis has led to significant unemployment and business disruption. While the government has provided massive programs aimed at supporting the broad economy, we expect ongoing market volatility and economic weakness until the virus subsides and more normal activity resumes.

Against this backdrop, we believe that certain sectors will be impacted more than others. To navigate these winding roads ahead, we remain steadfast in our disciplined approach of bottom-up credit analysis and risk evaluation. As always, we will continue to closely monitor our holdings, evaluate evolving risks and seek opportunities resulting from market dislocations.