Following the collapse of Silicon Valley Bank (SIVB) and additional stresses in the banking sector, the commercial real estate (CRE) market has been the latest sector to come under the microscope. The interdependencies between CRE and regional banks, coupled with weakness in the office sector and higher interest rates, have been cause for concern for commercial mortgage-backed security (CMBS) investors. In this piece, we explore the recent headwinds for CRE as they relate to regional banking and the office sector and shed light on our approach to deliver returns in this environment.

Connecting CRE to Regional Banks

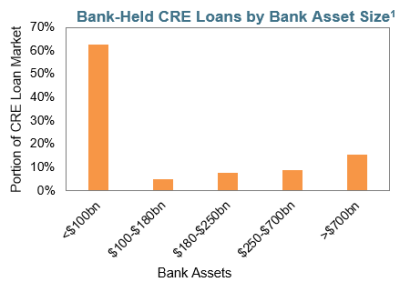

- The US banking sector’s importance to commercial real estate cannot be ignored as it finances roughly 40% of the total CRE debt outstanding. Larger-sized banks’ exposure to CRE loans is relatively small, owing to greater diversification across business lines and loan books. In contrast, a meaningful number of smaller-sized regional banks, particularly those with less than $100 billion in assets, have CRE exposures of 25% or more of their overall outstanding loans. The smaller banks account for a significant portion of total bank CRE lending.

- But not all CRE is created equal. The underlying property-level characteristics make all the difference when determining winners and losers as the details matter (central business district versus suburban, sunbelt versus coastal markets, unhedged floating rate debt versus fixed, and so on). While an older, more renter-affordable Class-B multifamily property could be resilient, a recently built, luxury Class-A asset facing greater new supply could face headwinds. These property-level risks are magnified for regional banks as they typically concentrate their commercial lending activities in their local geographies. This makes the margin for error much smaller when compared to larger banks.

- Post-FDIC interventions, the Federal Reserve (Fed) will begin to implement greater regulatory scrutiny on smaller-sized banks. Banks were natural buyers of highly rated CMBS tranches in their securities portfolios. Future regulations could force banks to hold more liquid, shorter duration, and lower risk securities, and result in the loss of a meaningful buyer of CMBS securities. This could pressure spreads, and ultimately the underlying CRE loans, as market participants demand a greater risk premium for holding these assets.

Credit Take: Is there a path forward for banks?

While not all CRE loans have been created equal, there remains a path forward for many cash flow-producing properties that ultimately may just have a valuation problem (i.e., higher interest rates resetting cap rates) rather than a fundamental problem (i.e., occupancy and net operating income (NOI) declines).

If NOI and property fundamentals remain intact, banks will be more inclined to make amendments and extend the loan maturity, preserving the value of their loan investment. The risk of banks taking control of CRE collateral stemming from maturity defaults, becoming forced sellers at fire-sale prices, is not a likely outcome.

As the market begins to separate the valuation issues from the fundamental issues, CRE sales transactions will come back to life as buyer and sellers adapt to the higher rate environment.

Addressing Office Sector Concerns

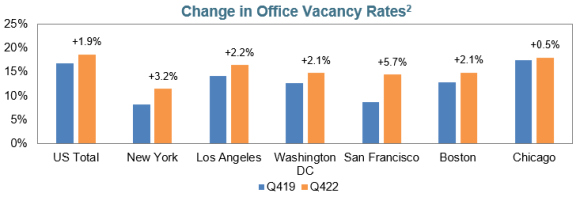

- The office sector has garnered its share of headlines recently. Not surprisingly, the sector is facing many headwinds from transitioning out of the COVID-driven work-from-home model into the hybrid model. Fundamentals have been challenged with the record pace of rate hikes, hiring freezes and tech sector layoffs, and a potential impending recession. This has resulted in slower rent growth – which has fallen to just 1% annually – and higher vacancy rates – above both pre-COVID levels and the 2010 peak.

- Property values will likely be pressured. Capitalization rates (the ratio of a property’s income to its market value) are important when estimating how property values could change. Cap rates have increased by roughly 1% but could increase further as more loans are refinanced at higher financing rates. Even if a property’s revenue was to remain constant, each 0.5% increase in cap rates equates to a 5% reduction in property values. However, more vacancies and slower rent growth will likely result in less revenue for each property. This has led to consensus estimates of at least a 30% decrease in office valuations over the next couple of years.

So, Where is the Silver Lining?

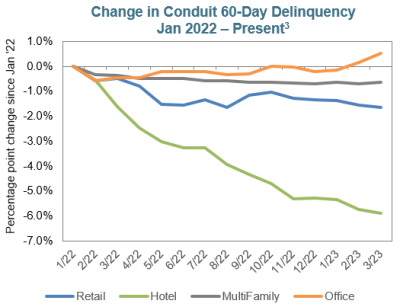

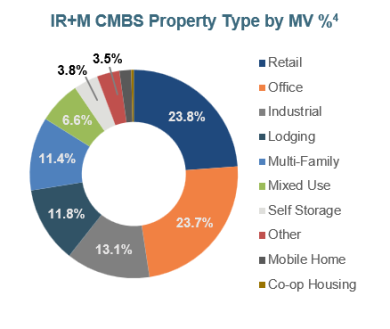

- The CMBS market represents more than just office properties. Office makes up a quarter of the CMBS market and is the only property type included in CMBS transactions experiencing growing delinquencies. However, this statistic can be deceiving, as not all office properties are facing the same level of challenges. Conduit CMBS transactions, which are the most common type of CMBS security, will also have varying exposure to office, multi-family, industrial, and retail properties, which helps mitigate the volatility from any one type. Investors can also further diversify their exposure through a mix of geographic locations.

- Lower property values do not equally impact all investors. Structure can provide significant protection against losses from forced property sales or property appraisal write-downs (for more information on conduit CMBS, please see here). Senior tranche securities can have credit enhancement or loss protection via subordinated tranches starting at 30%. The credit enhancement can grow to 40-50% on some seasoned senior securities through defeasance, loan payments, and amortization. Investors in senior tranches would therefore need property valuations across all sectors to fall significantly to experience any principal losses.

This Is Not Another Great Financial Crisis (GFC)

- CRE loans backing conduit CMBS are better positioned to withstand a weaker market cycle than the loans originated pre-GFC. Underwriting standards on CRE loans have tightened significantly since 2006-2007. Loan-to-value (LTV) ratios on recently originated loans are at least 10 points lower, which provides a much higher equity cushion to buffer potential valuation declines. This, combined with years of property value growth, limited foreclosures and liquidation activity, indicate CRE loans backing conduit deals are starting from a relatively healthy place.

- Deals are also more diversified. Investors have since demanded conduit CMBS deals have a more balanced exposure to different property types. While the broader CRE market was under stress during the GFC, only office is experiencing the majority of problems this time around. The higher diversification and relatively contained issues should give investors solace against losses.

- Some loans will still face headwinds. This will become more evident when borrowers try to refinance outstanding debt. However, the GFC taught us that loan modifications and patience with troubled assets generally produce more desirable outcomes. CRE lenders are more likely to extend and modify troubled loans, when possible, instead of foreclosing and liquidating.

IR+M’s CMBS Philosophy

- At IR+M we continue to focus on bottom-up security selection, concentrating on credit work at the loan level, stressing the structure with custom cash flow scenarios, and seeking to deploy liquidity at the right price. The market may paint the CRE market with a broad brush, but at IR+M, we do not.

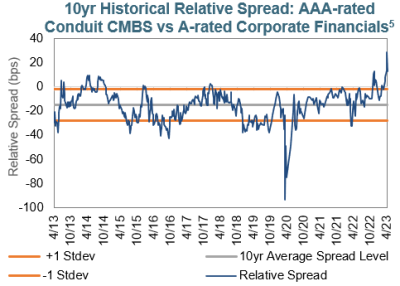

- We view current spread levels for senior AAA-rated conduit CMBS tranches as attractive relative to similar-duration corporate bonds, with the spread difference between the two sectors at the widest level in the last 10 years. Valuations appear even more attractive considering the credit enhancement embedded within senior tranches of conduit CMBS.

- However, spread volatility should persist given the growing uncertainties across markets. Headlines will continue to pressure conduit and SASB deals with high office exposure, but the initial widening due to the banking pressures seems to have peaked. A potential recession, the health of the consumer, and regional bank CRE lending will also impact the direction of spreads and the market’s ability to work through upcoming maturities.

The CRE market will likely remain in the headlines for the foreseeable future. While some scrutiny is warranted, we do believe that investors can navigate a volatile environment through bottom-up security selection and careful risk management. At IR+M, we favor senior tranches in well-diversified conduit CMBS securities with healthy credit enhancement. The structural advantages should help protect bondholders, even under distressed conditions, while offering attractive relative value to investment-grade corporates.