Charming the US Fixed Income Market: The Year of the Wood Snake

On January 29th, the world will usher in the Lunar New Year – the Year of the Wood Snake. In the Chinese zodiac, the snake embodies wisdom, caution, and enigma, while the wood symbolizes adaptability and renewal. As we shed 2024 and glide into 2025 – a period of transformation – we believe that the US fixed income market is a blend of cautious optimism and uncertainty. Like the wood snake, the market can appear subdued and safe, but it can also be enigmatic and strike without warning. For 2025, we anticipate the continuation of mostly stable credit fundamentals as we navigate potentially higher yields, modestly wider spreads, and robust supply. We also recognize that volatility-inducing events may be lying in wait – significant tariffs, increased animal spirits, and government-sponsored entity (GSE) privatization. Now more than ever, we believe that security selection is paramount as we traverse a landscape that may bend and twist in a myriad of ways.

On January 29th, the world will usher in the Lunar New Year – the Year of the Wood Snake. In the Chinese zodiac, the snake embodies wisdom, caution, and enigma, while the wood symbolizes adaptability and renewal. As we shed 2024 and glide into 2025 – a period of transformation – we believe that the US fixed income market is a blend of cautious optimism and uncertainty. Like the wood snake, the market can appear subdued and safe, but it can also be enigmatic and strike without warning. For 2025, we anticipate the continuation of mostly stable credit fundamentals as we navigate potentially higher yields, modestly wider spreads, and robust supply. We also recognize that volatility-inducing events may be lying in wait – significant tariffs, increased animal spirits, and government-sponsored entity (GSE) privatization. Now more than ever, we believe that security selection is paramount as we traverse a landscape that may bend and twist in a myriad of ways.

Wisdom: The Cautious Movement of the Market

With credit fundamentals and demand expected to maintain their stable trajectory, we are left wondering what 2025 will do for an encore. In the midst of this constancy, what we will not do is assume incomprehensible, uncompensated risk in our portfolios. Instead, we rely on the wisdom gleaned from our years of market pattern recognition. While the key themes may be reminiscent of those in 2024, we remain undeterred in our mission to scour the market for pockets of unrealized opportunity.

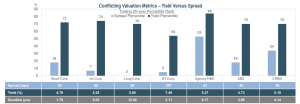

- The investment-grade market’s coiled tail could betray agitation. Investment-grade credit fundamentals are persistently sound, but they have likely peaked. The risk now is that companies remain overly optimistic and act aggressively with their balance sheets. Current spreads are not that attractive and may widen marginally according to dealer estimates. Yield levels are the more intriguing storyline. In recent months, expectations for interest-rate cuts have decreased significantly. Some pundits believe that the Fed may not cut rates at all in 2025. We attribute the 10-year’s recent upward trajectory to investors’ demanding higher yields given increased uncertainty around economic growth and inflation, as well as expectations of higher deficits.

The word on the IR+M desk. “It’s not to say that yields can’t go higher - they can. However, today’s starting yields provide a level of protection unseen in recent years and allow for additional upside in the event of any unexpected Fed cuts."

– Jim Gubitosi, Co-CIO, Senior Portfolio Manager

What we are doing. With sector dispersion and spreads at decade lows, we are still finding pockets of opportunity away from the more widely trafficked sectors and issuers. We believe that prudent security selection will be a key differentiator in a period where above benchmark returns could be more challenging.

- The high-yield market’s credit cycle conundrum. The high-yield market continues to have shades of investment grade, in that valuations are tight, and credit fundamentals are solid. With expectations of modest spread widening, low default rates, increased M&A, and easing financial conditions, investors are asking where we are in the credit cycle. Expansionary? Late? At IR+M, we believe that we are in the latter, which heightens the importance of prudent security selection. We anticipate that spreads will increase in the back half of the year in response to slower growth and mounting inflation, and that fallen angels will slightly outpace rising stars.

– IR+M Senior Research Analyst

- With the municipal market, all eyes are on supply. In 2024, the story coming out of the municipal market was its record-setting issuance, which exceeded $526 billion. 2025 seems poised for another strong issuance year, with an estimated $490 billion coming to market. Supply, which may exceed demand, could be accelerated due to concerns about potential tax reform and the absence of Covid relief funding. The proceeds of many transactions could be earmarked for deferred infrastructure improvements.

– IR+M Portfolio Manager

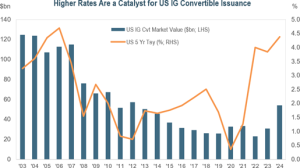

- Convertible bonds. Don’t call it a comeback. After falling in tandem with equities in 2022, convertible bond issuance has been on the comeback trail, accounting for $88 billion in supply in 2024. With rates on the rise, convertible bonds are an attractive means of lowering companies’ overall cost of capital and interest expense. Issuers typically benefit from convertibles’ lower coupon rates, which are below those of straight debt, and their recently streamlined accounting treatment.

– IR+M Portfolio Manager

Enigmatic: The Coiled Risks that Could Strike in 2025

With the US presidential election behind us, some investors assert that the markets’ multifaceted uncertainty has cleared. We believe that uncertainty will be a mainstay in 2025. In this year of change, we foresee an undercurrent of market disruption wrought by tariffs, increased M&A, and GSE reform.

- The US could move first with increased tariffs on February 1st. Or not. On the campaign trail, then presidential candidate Donald Trump threatened to enact a 60% tariff on all goods from China. On Inauguration Day, President Trump promised to impose additional tariffs of 25% on Mexico and Canada. The resulting average tariff rate could rise from 4% to 17.7%, the highest since 1934, which would escalate inflation, alarm markets, and constrict companies’ revenue streams. An estimated one-third of US investment-grade companies’ revenue is derived from China – the largest US trading partner – and increased tariffs could result in heightened inflation and margin compression. In this Year of the Wood Snake, targeted countries could respond with retaliatory tariffs of their own, setting in motion a global slowdown.

- Animal spirits are alive and well. While the Biden administration had been decidedly focused on anti-trust issues, the Trump administration has not. A more favorable regulatory environment would benefit M&A activity, and could trigger increased dealmaking and M&A-related issuance, particularly in high yield. In 2024, M&A issuance reached $200 billion; in 2025, it may surpass $210 billion. This resurgence is not without risk, as corporate balance sheets, which had been focused on defense and cost-cutting, are now shifting to offense and increased access to capital.

– IR+M Senior Portfolio Manager

- The GSE privatization wildcard. As the country’s 45th president, Donald Trump tried unsuccessfully to privatize Fannie Mae and Freddie Mac. As number 47, he may pick up where he left off. These GSEs, which were on the verge of collapse during the Great Financial Crisis, entered into conservatorship to stabilize the housing market. If the GSEs are privatized, we expect that mortgage rates will rise due to uncertainty related to government guarantees. Currently, if the GSEs experience financial distress, they, along with investors, will be bailed out by the government, which helps temper mortgage rates. With privatization, this guarantee – and lower mortgage rates – could disappear.

– IR+M Director of Securitized

Embodying the Wood Snake: The Year of Security Selection

We expect that 2025 – the Year of the Wood Snake – will be one of transformation in the US fixed income market, with significant policy and macroeconomic shifts driving volatility and modest spread widening. Embodying the wood snake, we believe that wisdom, caution, adaptability, and a focus on security selection will be essential as we navigate this complex and ever-evolving fixed income landscape.

We expect that 2025 – the Year of the Wood Snake – will be one of transformation in the US fixed income market, with significant policy and macroeconomic shifts driving volatility and modest spread widening. Embodying the wood snake, we believe that wisdom, caution, adaptability, and a focus on security selection will be essential as we navigate this complex and ever-evolving fixed income landscape.