Congress is negotiating additional economic stimulus in the throes of the financial repercussions of the COVID-19 crisis. While many corporations are focused on recovery efforts for their workforce and primary business operations, pensions can be a significant factor in the corporate bottom line. Pension funding relief will likely be a part of the ultimate agreement from Congress, and we believe history can be a helpful indicator in predicting the form this takes. In this mailer, we suggest the likelihood and form of pension relief, the potential adoption, and how long term funding statuses are likely to be affected.

LEGISLATION BLAST FROM THE PAST

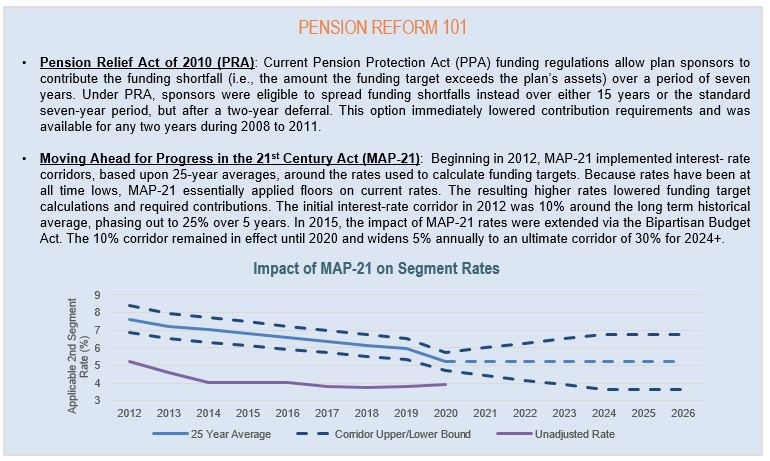

- There have been two notable occurrences of pension funding relief in the past decade – alternative amortization schedules under the Pension Relief Act of 2010 (PRA) and interest rate corridors introduced by the Moving Ahead for Progress in the 21st Century Act (MAP-21) in 2012. Both served to lower near-term contributions by smoothing and extending required contribution amounts. For an overview of these Acts, please refer to the Pension Reform 101 section.

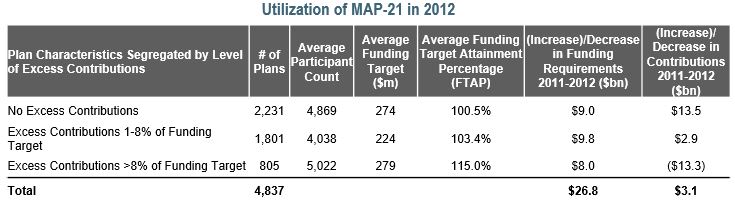

- The Society of Actuaries conducted a study in 2014 to understand how widely the contribution relief offered under MAP-21 was employed and they found that, while offered to all, only 46% of plan sponsors took full advantage of MAP-21 relief.

- The most underfunded plans were not the greatest beneficiaries; suggesting that perhaps other factors, such as higher priority corporate cash needs, drove their contribution decision making.

- At the other extreme, sponsors making the largest excess contributions were already generally better funded.

- The reductions of the first cohort were offset by the additional funding of the last cohort, resulting in an aggregate decrease in contributions of $3 billion from 2011 to 2012.

- Note: the Funding Target Attainment Percentage (FTAP) shown in the table above is used to determine funding requirements. This measure is not to be confused with the typically lower marked-to-market financial accounting funded status which better captures the economic reality of pensions.

TODAY I’M JUST A BILL

- As part of the CARES Act, 2020 plan-year required contributions can be deferred until after January 1, 2021. The Democratic controlled House recently passed the HEROES Act in May. Senator McConnell called the bill “dead on arrival” and it is unlikely to pass the Republican controlled Senate. The HEROES Act did include two pension relief provisions, modeled after PRA and MAP-21 – allowing for a 15-year amortization schedule and narrowing interest-rate corridors to 5% of 25-year historic averages until 2025.

- While the passage of the HEROES Act is improbable, Congress is under pressure to pass additional economic stimulus. Pension relief is likely to be included as it tends to have bipartisan support. Lowering required but tax-deductible contributions is a win-win – it provides relief for plan sponsors, while increasing tax revenues for the Federal Government.

2012 VERSUS 2020

- In 2012, the economy was in a position of growth – with positive equity market returns and GDP growth. The COVID-19 crisis has challenged the start of 2020 with volatile equity returns, negative GDP growth, historic low inflation, and record high unemployment – levels not seen since the Great Depression. There is growing consensus that we are in a recession.

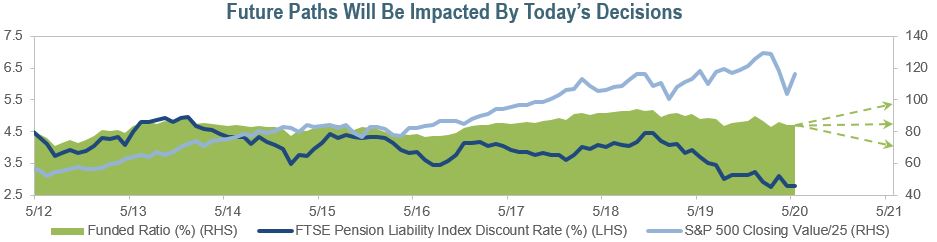

- Funded ratios (measured on a marked-to-market based discount rate, as opposed to smoothed interest rates used for determining required contributions in the prior section) have steadily improved over the last eight years. Despite historic low discount rates, assets have been buoyed by positive returns and dedicated cash contributions (further accelerated as a result of the 2018 tax reform).

- The state of defined benefits plans and the economy are very different today than they were when MAP-21 was introduced in 2012. Given the current economic environment, which could have lasting detrimental impacts on businesses, we believe there is potential for greater take-up of any pension relief compared to 2012.

OUR OUTLOOK FOR 2020 AND BEYOND

- We believe there is bipartisan support to pass funding relief before the next tax-filing deadline in 2021. Many businesses have a need for liquidity and would benefit from diverting cash towards core operations in the short term. Contribution-related legislation also benefits the Federal Government (whose debt continues to grow) by providing tax income.

- A number of sponsor-specific factors will influence the degree to which sponsors take advantage of funding relief, if at all.

- The most dominant driver of their decision will likely be their overall financial position, including the need to cover ongoing expenses, depressed revenues, and limited free cash flow available.

- Considerations that may dissuade sponsors from deferring contributions include: a significant pension deficit relative to the overall corporate balance sheet, a desire to make continued progress towards an upcoming pension risk transfer or plan termination, and having earmarked and committed to making 2020 pension contributions.

- However, we believe the economic environment will weigh more heavily on businesses in 2020 than in 2012. Businesses in those sectors that have been hurt most by the virus, such as airlines, colleges, hospital systems and automobile manufacturers, will likely prioritize immediate cash needs to keep businesses afloat above funding their pensions today.

- The path of pension funding statuses is impacted by: funding decisions, the chosen investment strategy and its associated risk tolerance, levels of interest rates, and the timing and form of a recovery. A strong and sooner-than-expected recovery could lead to flat or even increases in funded status regardless of contribution deferrals today.

- A pension’s funded status will likely suffer if contributions are reduced or deferred. Sponsors may consider re-risking their asset allocation from fixed income to return-seeking assets to grow out of their pension deficits, perhaps lowering demand for buying bonds. However, corporate bond issuance flooded the market in 2020 and has been met with equally strong demand, indicating an appetite for Liability Driven Investing (LDI) to combat market volatility. With the impact of COVID-19 likely to linger, employing LDI could ease the risk of a growing pension deficit should recessionary trends continue.

- We believe there will be a “new normal” that evolves and LDI can provide downside protection in the face of this uncertainty and continued volatility. If history can serve as a cautionary tale, in 2018 discount rates and funded status levels peaked at 4.4% and 94% respectively. Rates have steadily dropped since, and sponsors who adopted LDI could have prevented future funded status losses and reduced contributions.

It is unclear how severe market impacts from COVID-19 will be and how the Federal Government will ultimately enact stimulus. While contribution relief is much needed by corporations who have been negatively impacted by COVID-19, we believe an unintended consequence may be a trend of depressed funded status levels. The hope is that markets eventually reverse and sponsors emerge in a better position to make those contributions when they come due. At IR+M, we are committed to partnering with our clients as they navigate these uncharted waters and communicating our insights to help guide their decisions.