“May you live in interesting times” — ancient phrase of unknown origin.

First issued in 1997, TIPS are still the new kid on the U.S. Treasury block. But over the past 23 years, investors have embraced TIPS for their unique combination of inflation protection and risk-free credit. These investors are paid on the incremental changes in the Consumer Price Urban Non Seasonally Adjusted Index as published by the Bureau of Labor Statistics. That’s a mouthful. But this “inflation float” can be a powerful strategic diversifier in broad investment portfolios as well as a tactical best idea in nominal fixed income strategies when “interesting times” befall us.

Quick refresher: TIPS trade off the ‘real yield curve’. The real yield curve has no direct relationship to the U.S. Treasury nominal yield curve. This is important because it has implications for computing risk metrics such as duration and convexity. The mathematical difference between the real and nominal yield curves is the ‘breakeven curve’. A break-even at a given maturity point is the average annualized inflation (per the index above) required for the carry on a TIP security to match the yield to maturity on a U.S. Treasury. The mechanism for TIPS to accrete inflation is through the index ratio. Positive inflation increases the TIPS ‘index ratio’ and negative inflation (deflation) decreases it. This index ratio is a multiplier for all TIPS principal and interest payments. Interestingly, a TIPS holder will not receive less than par at maturity even if inflation was net negative (i.e. deflation). This feature is called the TIPS “deflation floor” and it insures TIPS are treated no worse than nominals in principal repayment dollars.

TIPS real yields provide important market information. They are pure discount rates for the time value of money in the same way that real GDP is the pure rate of economic growth. They also provide a comparative measure for interest rate parity around the globe. Real yields can and will trade below zero, which is not a recrimination on TIPS, but a byproduct of an overall suppressed interest rate environment. Unfortunately, negative real yields also mean that the earned inflation is less than whole for the investor. I find this ironic: investors must pay the government a cut for protection against their inflationary policies.

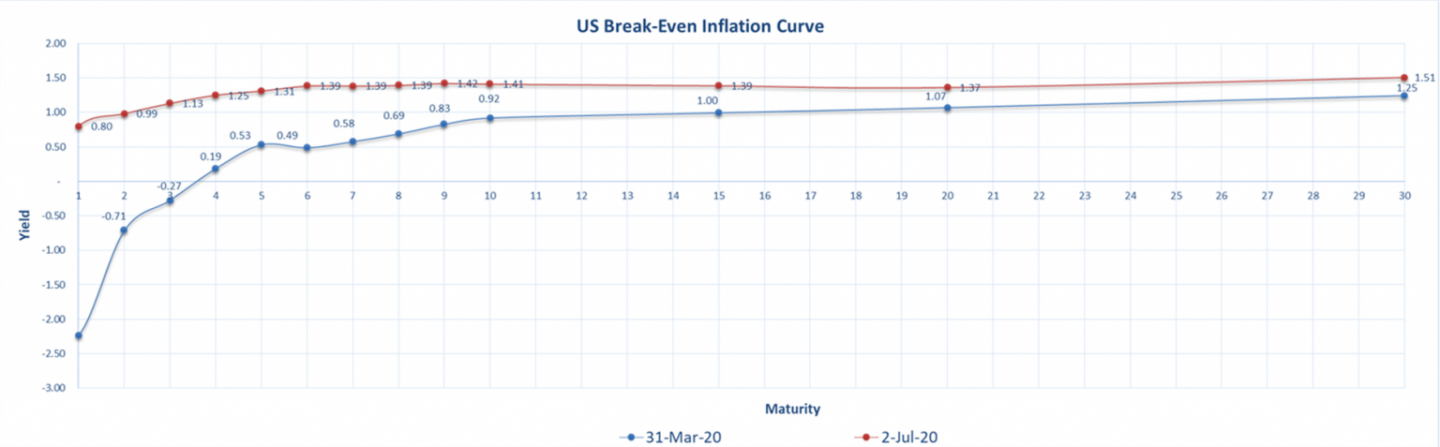

The breakeven curve tends to rise and flatten during periods of high inflation and decline and steepen during periods of low inflation (see chart below). Break-evens further out the curve (e.g. 7+ year maturities) have historically traded in a relatively tight range. However, break-evens in the belly of the curve (e.g. 4-6yr maturities) have traded with far more volatility. When TIPS break-evens are dragged down by deflation fears, belly maturities offer a combination of low break-evens and ample time to maturity for inflation to recover. At times, front-end TIPS maturities (0-3yr) have traded with especially downtrodden break-evens (sometimes at or below zero), but they have higher index ratios and limited time to recover before maturity. If I could advise the Treasury on one new security type, it would be a two-year TIP security; the liquidity and deflation floor of a short on-the-run might mitigate excessive volatility in front-end break-evens during “interesting times”.

(source: Bloomberg)

Like Cholesterol, inflation comes in two forms. ‘Good’ inflation is a byproduct of a taught and robust economy – wage growth, resource competition, and capital investment pushing prices steadily higher. In this case, most high-quality fixed income faces return headwinds from rising interest rates. But with a strong economy, credit spreads are likely tightening while break-evens expand, causing TIPS to look and act a lot like spread product at the portfolio level. On the other hand, ‘bad’ inflation is a byproduct of a weak currency – volatile commodity prices, economic uncertainty, and labor unrest push prices higher in an unpredictable manner. This ‘stagflation’ is a headwind not only for nominal interest rates but also for credit spreads. However, real rates are likely to remain low while break-evens widen – making TIPS a unique and powerful diversifier in the portfolio.

The catalysts for inflation are largely mysteries. Fed officials have admitted to such over time. Ideally they’d be able to peg core inflation at 2%, but this hasn’t been the case in recent years. Forward break-evens are a means to gauge investors’ long-term expectations for future inflation. For this reason, the Fed keeps a watchful eye on 5yr x 5yr forward break-evens, extrapolated directly from the TIPS market. When the 5x5yr break-even dips below 1.5%, Fed officials tend to get nervous. That is where it is now.

So what is a fixed income investor to make of all this? TIPS are not found in traditional benchmarks. They trade off a different yield curve. They accrue inflation float to their principal component. That principal component will never be paid out at less than par. All of this argues for TIPS to be treated as a separate asset class, with a distinct allocation and benchmark in a broad investment portfolio. Those arguments make sense to us.

But TIPS also share technicals with nominal fixed income. TIPS comprise less than 10% of marketable Treasury debt outstanding, so liquidity waxes and wanes relative to that of their big brother. We believe opportunities to tactically add TIPS in nominal fixed income strategies are compelling when deflation fears and liquidity concessions have pushed break-evens close to zero. The key is in the belief that inflation will return, either in the “good” form (from a robust economic recovery) or in the “bad” form (from aggressive monetary loosening). Either way, the TIPS investor wins with patience. Of course, once inflation does recover, holding TIPS relative to other spread product becomes less compelling. And if a prolonged period of negative inflation really does beset us, TIPS have the deflation floor and U.S. Treasury credit profile as protections. All of this makes TIPS look good to a bottom-up fixed income manager even if the macro-economic outlook is clouded by “interesting times”.