All year, investors have been questioning if now is the time to extend their cash. While money market funds have remained attractive given the recent higher yields, particularly at the front end of an inverted curve, the market continues to watch for signs that the Fed is ready to cut rates. Should these rate cuts materialize, money market yields and returns could fall quickly. Investors who modestly extend duration and diversify their exposures can benefit in this environment, while still preserving their yield, liquidity, and principal.

An extended cash portfolio* utilizes an expanded maturity spectrum and typically has more diversified holdings versus a money market fund. With a portfolio customized for their liquidity, an investor can also lock in current rates for longer.

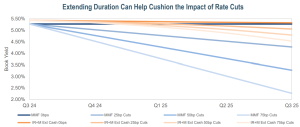

Yields Remain Elevated...

- Although the market was pricing in numerous cuts at the beginning of the year, the Fed has continued to hold rates steady.

- Money market funds continue to see record balances, with investors earning over 5% on their cash. If interest rate cuts materialize, these returns are expected to decrease rapidly, making the case for strategically extending cash to lock in the higher rates.

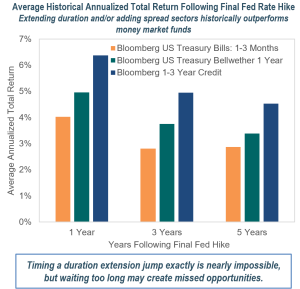

- While perfectly timing your duration extension jump is nearly impossible, waiting too long may create missed opportunities.

... But Rate Cuts Still Loom

- The most recent CPI report - one of the Fed’s most-watched data points - came in below expectations, increasing the likelihood that the Fed could cut rates in September if ensuing reports follow a similar trend.

- Many of the major central banks have started to cut rates, including the European Central Bank, with expectations for the Bank of England to soon follow. Current market pricing indicates that this policy divergence with an on-hold Federal Reserve should not persist for long.

- The current yield curve inversion is the longest inversion recorded and has led money markets to look attractive on an absolute and relative basis. However, this may be giving money market investors a false sense of security if (and when!) rate cuts occur and we return to a more normalized curve.

- Money market funds (blue lines above) and IR+M’s Short Extended Cash portfolio* (orange lines) yields are currently aligned, but assumed rate cut shocks show the wider range of scenarios for a shorter duration money market fund.

- If rate cuts happen, money market funds will feel the impact almost immediately and have more downside risk.

- Extending duration and diversifying holdings can help to lock in the high rates for longer, thereby softening the impact of rate cuts and protecting against the downside.

- Aligning portfolio construction with known liability and liquidity needs can further optimize returns.

Better to be Early Than Late

While the market continues to contemplate the timing and magnitude of potential rate cuts, yields remain elevated and spreads in the short end provide a robust opportunity set.

Extending cash from money market funds ahead of a rate cut can lock in these higher yields for longer, capture total return, and provide additional diversification while maintaining liquidity options.

In addition, the current yield environment provides a cushion against any future rate increases. Front-end rates would need to rise by over 500 basis points for the 1-Year Treasury Bellwether Index to return 0%. Additional cushion is obtained with the inclusion of spread product.

Enhancing Your Cash

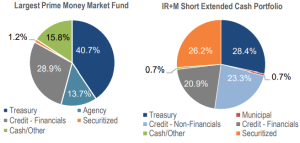

Money market funds typically have concentrated positions in select government issuers and counterparties. While these are high quality exposures, they may be susceptible to extreme volatility, particularly in the overnight markets.

IR+M’s Short Extended Cash strategy is well-diversified across Treasuries, corporate bonds, securitized assets, and municipal bonds. The strategy aims to mitigate investment and credit risk via short maturity, high-quality, investment grade ideas and thorough bottom-up credit research. The strategy can also be customized to meet specific requirements or preferences.

Money market reforms adopted by the SEC require increased liquidity buffers, allowing prime funds to impose liquidity feesand temporarily suspend withdrawals in certain circumstances. IR+M offers the flexibility to liquidate a portfolio at any time and can work with clients to customize portfolios to meet specific, known cash flow needs to optimize market exposure and minimize transaction costs.

At IR+M, we do not predict interest rate moves when managing our portfolios. However, the market and the Fed continue to indicate the likelihood of a rate cut in 2024 and many clients have contemplated a move out of their excess cash accounts. Given current yield levels, we believe that there is limited downside risk to moderately extending duration and caution against waiting too long to take that jump. Don’t let your cash drag you down - getting ahead of the expected interest rate cut(s) can provide investors with similar yields and the opportunity to benefit when rates fall.