TIPS as Spread Product

IR+M clients know that we go out of our way to avoid betting on the direction of interest rates. We work from the bottom up, carefully selecting and weighing specific securities (and by extension, sectors) to drive portfolio returns. The last thing we want in client portfolios is security-specific excess return wiped out by a wayward rate bet.

Our clients also know that we avoid specific positioning for inflation. Or is it deflation? The current narrative seems split between hyperinflation, via seismic shifts in monetary and fiscal policy, and a deflation death spiral, stemming from too much indebtedness (private and government) and low money velocity. Which is it? And how will it unfold? Over what period? The more popular narrative since the Great Financial Crisis has been inflation, and if you have been positioned for it in TIPS and many commodities, you have been wrong. As such, it should be no surprise that we view inflation positioning as another one of those alpha eating macro bets.

So why do we hold TIPS in client portfolios? Because they are cheap! Looking at TIPS through the lens of “spread product” (securities that trade with a ranging spread relative to Treasuries), we can find compelling reasons to capitalize on opportunities in the space.

Treasuries with a Liquidity Problem (Sometimes)

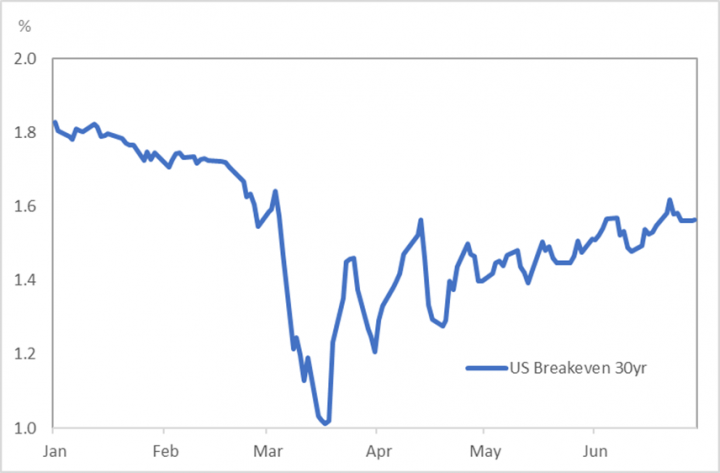

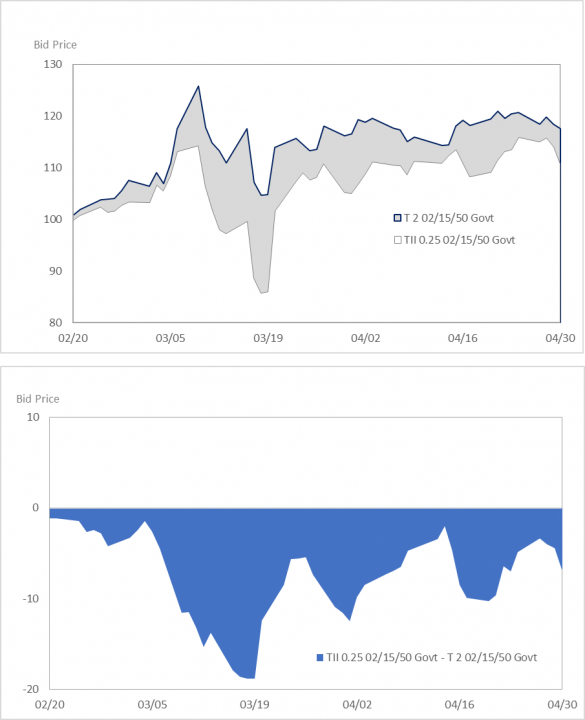

In the three weeks leading up to March 23rd (the date that the Fed announced its multitude of emergency lending facilities), US bond market liquidity was likely the worst experienced since late 2008. Markets were so volatile that Wall Street Treasury traders were rumored to have “turned their computers off” (automated small lot and Off-The-Run trading) to avoid getting caught offsides during the tumult. The deepest, most liquid market in the world shifted its focus to exclusively trading On-The-Run securities. Relative to On-The-Run nominal Treasuries, prices for Off-The-Run Treasury and TIPS securities plunged while bid/ask increased. For example, Off-the-Run 2048 Treasury issues underperformed the February 2050 On-the-Run issue by $4 points/400bp in the trading days between March 9th and March 19th. Long dated TIPS fared much worse.

The February 2050 TIPS issue underperformed its maturity-matched nominal Treasury peer by close to $20 points/2000bp at the worst point. To be sure, the market was baking in UGLY forward economic expectations, but that was not the whole story. Our experience trading TIPS at that time (frozen markets!) told us that the price action was being more heavily influenced by liquidity than by inflation expectations. Having seen this happen to the TIPS market in 2008, 2011, 2015, and 4Q18, we judged the liquidity disruption to be an appealing entry opportunity, so we stepped in and bought.

30-Year Breakeven Yields (Nominal Treasury Yield – TIPS Yield)

February 2050 TIPS Price vs February Nominal Treasury Price

A Tradable Spread with No Knockout

What do we typically do when we see a corporate bond offering a credit spread that is “cheap” to its long-term range, while still being fundamentally sound? We buy it. The reverse is also true; we pare back on the tight spreads. The “gotcha” in credit spread trading is that fundamental erosion, landscape change, and downgrade risks are real. Corporate bond spreads must compensate buyers for these inherent credit risks, among others. Not all wide spreads are a slam dunk; unfortunately, some wide (and attractive) spreads go wider.

What if we could find a tradable spread with far less, or no, idiosyncratic credit risk? What about a spread trade that could be increased in size prudently if it moves against you? Are there bonds that become cheap in the absence of downgrade/bankruptcy risk? How about TIPS?

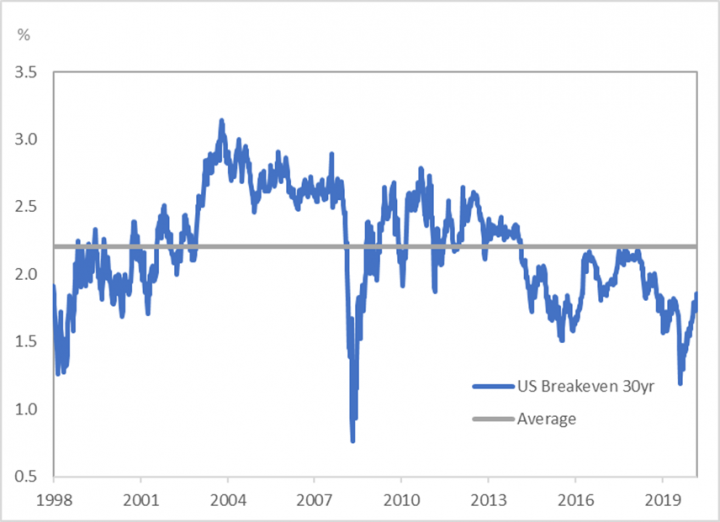

As seen above, TIPS breakevens are influenced by liquidity in the short run. In the long run, breakevens appear to be highly influenced by the Fed’s 2% inflation target, and tend to trade in a range around that target. If timed and sized appropriately, TIPS trades can be as successful as the best corporate bond trade, but with much less idiosyncratic risk.

Unlike corporate bonds, where we want spreads to go tighter (lower), TIPS buyers want breakevens to move higher. Higher breakevens are a signal that TIPS yields are increasing their distance from nominal Treasury yields. If you can get past thinking about the spread the opposite way, managing risk and harnessing opportunity in the TIPS market has many parallels to doing the same in other spread product (corporate, securitized, municipal) markets. The key difference is that outside forces (rating agency downgrades, competition, and defaults) can’t bounce you from your trade or turn you into a forced seller.

A Long History of 30-Year TIPS Breakeven Spread

In Summary

At IR+M, we avoid betting on the future of interest rates or inflation, but we aren’t afraid to take advantage of a market dislocation that presents alpha opportunity. We feel, the TIPS market allows us to do what we do best – obsess about risk- adjusted relative value from the bottom-up, and transform that obsession into return-generating investments for our clients.