Insurers continue to grapple with low rates and search for ways to add yield in this environment. While overall portfolio allocations were stable in 2020, there were several noteworthy allocation moves, including a continued decrease in municipals and growth within NAIC 3-rated securities. In our third annual analysis of insurance company filings, we examine the impact of these trends and changes both in 2020 and going forward. We also explore how insurers can navigate this low-yield environment without moving too far out on the risk spectrum.

2020 Allocation Lookback

- Despite the volatility in 2020, insurance company investment portfolios benefitted as markets bounced back from the initial shock of the global economic shutdown and ended the year with strong performance.

- Total cash & investments was up $503 billion to nearly $7 trillion. We continued to see an increase in unrealized capital gains, which was up by $53 billion on the year.

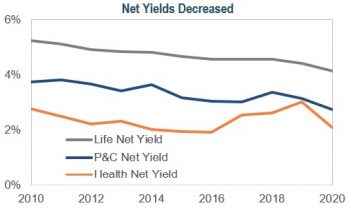

- In response to a significant decline in Treasury yields, net yield on invested assets fell by the largest amount in over 10 years. Property & Casualty (P&C) and Life net yields were at the lowest levels on record.

- Overall asset allocation moves within insurance company investment portfolios were small and primarily around the edges. Within P&C, equity allocations ended the year at their highest levels ever, while bonds were at their lowest.

- Within bond portfolios, corporates remained the predominant allocation and were up slightly across insurance lines during the year. Allocations to securitized bonds were relatively unchanged. P&C and Health insurers also continued to reduce their municipal allocations, an ongoing theme since the passage of the Tax Cut and Jobs Act (TCJA).

Municipals Look Expensive Versus Other Alternatives, Even Considering Future Tax Rate Changes

- The Biden Administration has proposed several tax changes, including increasing the corporate tax rate from 21% to 28%, though a 25% tax rate is also being discussed.

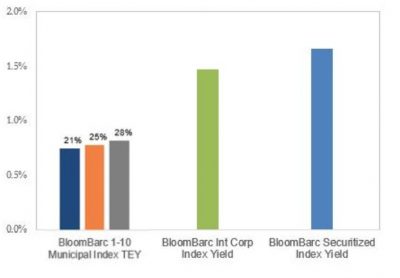

- Although higher tax rates benefit municipals relative to other taxable options, even if tax rates were to rise, the higher municipal taxable-equivalent yields (TEY) would still fall short of corporate and securitized yields, as historically low municipal yields have diminished the value of the tax exemption.

Fixed Income Ratings Observations

- While sector allocation changes were modest year-over-year, ratings exposure within fixed income portfolios shifted meaningfully. Allocations to NAIC 2 securities steadily climbed in 2020, and there are several trends that could lead to even higher allocations in 2021.

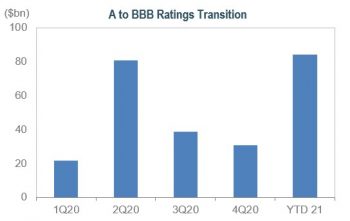

- Year-to-date in 2021, the largest investment-grade ratings migration has been from single A to BBB-rated securities, with some companies willing to risk a downgrade for M&A transactions. Over $80 billion was downgraded through early April, compared to $170 billion total in 2020.

- The spread difference between A and BBB-rated corporates is well-below long-term averages. This, combined with broadly tight spread levels, may further disincentivize companies from maintaining their A ratings.

- The BBB-rated universe has also seen almost $21 billion in growth from rising stars (high-yield bonds upgraded to investment grade).

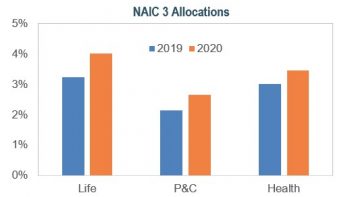

- NAIC 3 allocations also rose during the year, reaching their highest levels in the last five years across all insurance company types. Fallen angels (investment-grade bonds that have been downgraded to high yield) likely contributed to the increase. Although short of initial projections, there were still $185 billion in 2020, the highest calendar year total on record.

- Looking ahead, the BB universe may offer opportunity to insurance companies looking to maintain portfolio income.

- The proposed changes to Risk Based Capital (RBC) bond factors would, among other things, increase the capital efficiency of bonds rated BB+.

- Although BB spreads have tightened significantly over the last year, they remain wide to BBBs.

- Fallen angels have also expanded the size, quality, and duration of the opportunity set.

Navigating the Low Yield Environment

- Many of the shifts in insurance company portfolios have been in response to the low interest rate environment.

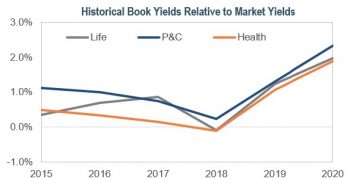

- The difference between book yield and the current fixed income market yield is at a recent high. As these higher-yielding assets mature, insurers may be forced to re-invest at lower yields, putting further pressure on investment income.

- Insurers might consider revisiting 144A investment guideline limits when possible. 144A securities are a significant portion of the universe, accounting for over 25% of investment-grade corporate new issue in 2020, and almost 60% of asset-backed securities (ABS) new issue. In addition, 144As have better liquidity than true private placements.

- Opportunity also remains present in the securitized sector, particularly in ABS and commercial mortgage-backed securities (CMBS), which can offer more attractive spreads, yields, and capital treatment than similarly-rated corporate bonds.

The Evolving Securitized Universe

- The securitized universe has expanded beyond the typical auto- and credit card backed-securities, and now

includes many non-traditional sectors that we believe can offer insurers higher yields than similarly-rated corporates and municipals, diversification benefits, and better structural protections.

includes many non-traditional sectors that we believe can offer insurers higher yields than similarly-rated corporates and municipals, diversification benefits, and better structural protections. - Railcars: Goods and commodity flow was consistent during the pandemic, and railcar ABS did not experience significant delinquencies or decline in utilization.

- Datacenters: The majority of tenants are investment grade and turnover is low given essential business needs and high switching costs.

- Whole Business: Franchise agreements are long-term with a fixed rate, backed by franchisee fees and royalty income, and provide a stable cashflow.

- Collateralized loan obligations (CLOs): The structural strength has proven out over multiple credit cycles, and heavy year-to-date supply has led to wider trading levels.

- Vintage conduit CMBS also offers value in the short end given enhanced credit protection with minimal prepayment volatility. Recent NAIC changes have led to some adverse scenario analysis for lower-rated tranches, which resulted in modest spread and selling pressure within the sector. Despite this, we believe there are selective opportunities, and with a diversified, up-in-quality approach, CMBS can provide attractive relative value.

At IR+M, we believe that, despite the low yield environment, there are investment opportunities within fixed income that offer relatively attractive risk-adjusted yields, such as the securitized sector. We believe that bottom-up security selection is paramount in this environment, especially since impairments can quickly reduce returns. Through our experience managing fixed income portfolios and partnering with insurance clients, we think we are well-positioned to help fulfill investment needs in this low yield environment.