The coronavirus pandemic has spared very little, including state and local government finances. These entities must now find a way to balance rising healthcare and unemployment costs with declining tax revenues. The rating agencies have taken notice, with S&P recently placing every municipal sector on negative outlook. In previous cycles, this time-tested market has withstood bouts of volatility, downgrades, and even the occasional default. We believe that the municipal market has stabilized, bolstered by its taxing and semi-sovereign authority, and that it will continue to perform well for investors.

AN ASSIST FROM THE FED

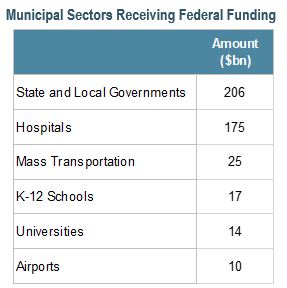

- The Federal Reserve (Fed) and US Congress have leveraged their prior recession experience, and responded swiftly to the current economic crisis. The $2 trillion CARES Act was signed into law in March 2020, and has provided billions of dollars in relief to several municipal sectors, including hospitals, state and local governments, higher education, public transit, and airports.

- Thus far, the Fed’s stimulus programs have neglected to include support for smaller cities and rural areas. Help could be on the way for these entities. While the funding may not be a panacea, it could alleviate some financial pressure.

- We expect that some municipal issuers will continue to struggle, and that downgrades (not necessarily defaults) will occur in the upcoming months. As history has shown, in the municipal market, perception is not always reality. While there are areas of risk, there are also areas of opportunity.

HIGHLIGHTING THE RISKS

Most At-Risk: Senior Living, Convention Centers, Hotel Occupancy Tax Bonds, and Non-Essential Lease Debt

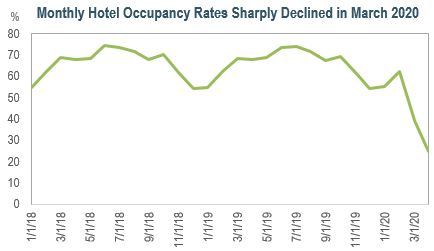

Pervasive lockdowns have resulted in sharp travel declines, and therefore dramatically lower hotel occupancy levels. Occupancy rates have approached 20%, which could pressure those bonds secured by convention center and hotel tax receipts.

Pervasive lockdowns have resulted in sharp travel declines, and therefore dramatically lower hotel occupancy levels. Occupancy rates have approached 20%, which could pressure those bonds secured by convention center and hotel tax receipts.- Narrow-based – or non-essential – leases may be in jeopardy now more than ever. Lawmakers could face difficult appropriation decisions for projects with revenue – and ultimately debt service payment – shortfalls.

- For example, lawmakers in then AA-rated Platte County, MO, failed to appropriate funding to pay debt service on the stressed Zona Rosa Retail Project bonds. Legislators deemed the project to be non-essential, which caused the project to default on its debt payment.

- We believe that it is important to assess the extent of a lease’s essentiality. Lease bonds with higher essentiality and strong bondholder covenants, such as robust debt service coverage ratios, reserve funds, and additional bonds tests, may be worth considering.

Medium Risk: Airports, Hospitals, Higher Education, Toll Roads, Public Transportation, Tax-Backed General Obligation (GO) Bonds, Sales and Special Tax Bonds, and Essential Asset Leases

- State and local GO issuers that failed to build reserves or reduce pension liabilities during the last economic expansion – or are heavily energy dependent – may be moderately risky.

- Numerous colleges and universities are facing enrollment uncertainty in the fall of 2020. Many students who pay full tuition are considering deferring for a year. Also, with several states facing budget shortages, appropriations to public colleges and universities could fall.

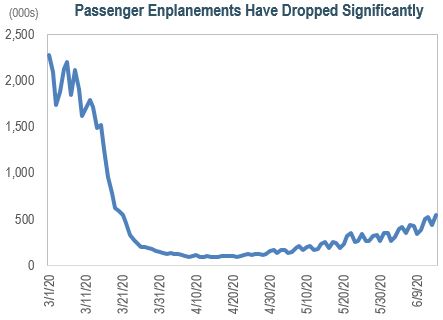

- Transportation sector fundamentals continue to deteriorate. Passenger enplanements have dropped 79% y/y, and toll road traffic has fallen by 50%. Public transit ridership has plunged more than 90%.

- The healthcare system has been strained, with hospitals experiencing a simultaneous surge in ICU patients and decline in elective procedures.

- We believe that size is a key differentiator in municipal credit. Issuers experiencing acute pressure tend to be smaller with narrow revenue streams; larger issuers often have more flexibility. Sales and special tax bonds with strong covenants, highly-rated hospitals and colleges with robust reserves, and beneficiaries of the CARES Act may also be worthy considerations.

Lower Risk: Utilities (Water & Sewer) and High-Quality GOs

- Utilities that operate in tourism-dependent regions, like Orlando, FL, may depend on a few customers (like Walt Disney World) for the majority of their revenue. Utilities that serve industrial-focused areas may be similarly reliant on a small number companies for income.

- The good news is that utilities are often viewed as the bedrock of the municipal market. They provide an essential service, which is reflected in their typically high credit ratings. Management teams often can unilaterally raise rates to meet debt service, or execute utility-friendly take-or-pay contracts.

- High-quality GOs are another example of a safe haven sector. These GOs are often characterized by consistent and diversified revenue streams, strong reserves that can mitigate budget deficits, and well-funded pensions.

ISSUERS MAKING HEADLINES

Metropolitan Transportation Authority (MTA) (A2/A-/A+/Negative)

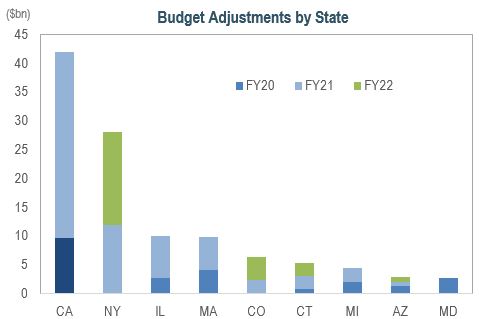

- The MTA, which is New York’s essential service transportation provider, has an estimated $45 billion in debt, and is one of the municipal market’s largest issuers. State legislators recently voted to raise the MTA’s borrowing capacity to $90 billion. The MTA may borrow up to $10 billion to finance operating costs from 2020 to 2022.

- The MTA, unlike its airport and toll road counterparts, does not have a strong balance sheet or liquidity. In addition to being overleveraged, MTA has an extensive capital expenditure backlog. With ridership down 90%, the MTA is burning an estimated $150 million in cash a week.

- Despite the MTA’s sizable debt burden, we believe that the state, as well as the federal government, will continue to provide emergency funding. We expect the MTA to remain financially strained, and at risk of a downgrade.

State of Illinois (Baa3/BBB-/BBB-/Negative)

- Illinois has one of the worst funded pension systems – and debt burdens – in the nation. We anticipate that its financial stress will endure, given its deteriorating pension funding ratio, increasing liabilities, and ever-present bill backlog.

- Illinois state legislators are constantly pressured to cut expenditures and raise taxes. The state’s governor and General Assembly are finally aligned politically, which could make these discussions less contentious.

- We believe that the rating agencies will maintain Illinois’ rating until the November 2020 election, which will feature a progressive income tax amendment on the ballot. If the initiative fails, the rating agencies could downgrade the state to high yield – a first for any state.

- We feel that a downgrade to high yield would raise Illinois’ borrowing cost, but not affect its ability to service its debt. It is important to recognize that under the US Bankruptcy Code, states are forbidden to declare bankruptcy. Changes to this code would require an act of Congress, which is unlikely.

State of New Jersey Appropriated Debt (Baa1/BBB+/BBB+/Negative)

- We believe that New Jersey’s challenges are similar to those of Illinois – elevated fixed costs, a poorly funded pension, and minimal reserves.

- The state’s fiscal 2019 financial results surpassed expectations. It was on track to end fiscal 2020 with a budget surplus, but recent economic events could alter that outcome.

- New Jersey’s tax rates are among the highest in the nation, which makes future tax increases unpalatable for politicians and residents. As a result, the state may have to use short-term borrowing to close projected budget gaps for 2020 and 2021.

- While we believe that New Jersey will maintain its investment grade rating, a prolonged downturn could trigger a downgrade to low investment grade.

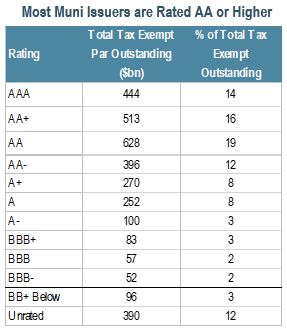

At IR+M, we believe that principal protection is paramount. Our portfolios, which have an average rating of AA, reflect our up-in-quality bias. We rely on our experienced credit research team to uncover essential purpose issuers that we feel can withstand economic volatility. Over the next year, we expect that most municipal issuers will continue to contend with the aftermath of the coronavirus pandemic. Yet we believe in this market’s resiliency, and in our ability to identify sound investments that will endure and outperform.