In our annual analysis of insurance company filings, we examine trends and changes that occurred in insurance companies’ investment portfolios during 2021. As is typically the case, overall portfolio allocations were relatively stable, but we did notice some noteworthy shifts on the margin. We also highlight some investment opportunities for insurance companies in a rising interest rate environment.

2021 Allocation Lookback

- Total cash & investments grew $456 billion or approximately 7% year-over- year, reaching a record of over $7 trillion, and marking the third consecutive year of annual growth of 7% or greater.

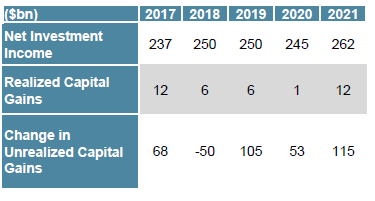

- Despite the continued low interest rate environment in 2021, net

investment income and unrealized capital gains also reached record highs of $262 and $115 billion, respectively, aided by the higher equity allocation within Property & Casualty (P&C) companies.

investment income and unrealized capital gains also reached record highs of $262 and $115 billion, respectively, aided by the higher equity allocation within Property & Casualty (P&C) companies.

- Overall asset allocation shifts were small and on the margin. P&C ended the year at another all-time high for equity allocations, likely driven by strong equity market returns in 2021, while bonds reached their third consecutive low.

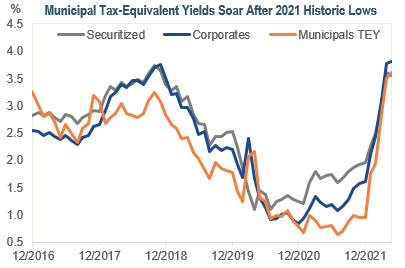

2021 Allocation Spotlight: Municipals – The Darkest Light Before the Dawn

- P&C and Health insurers continued to decrease their municipal bond (muni) allocations in 2021 given historically low muni yields which diminished the value of the tax exemption. In 2021, muni/Treasury ratios reached historic lows and munis looked expensive relative to many taxable options. Year-to-date, however, we have seen a reversal with muni/Treasury ratios rising significantly, presenting an attractive relative value opportunity to add back to the muni sector.

- As rates have risen this year, the value of the tax exemption has also grown. Munis tend to outperform in a rising rate environment so the attractiveness of the asset class is returning and we believe insurer’s muni allocations will stabilize.

Fixed Income Observations

- Overall credit quality based on the National Association of Insurance Commissioners (NAIC) designations remained stable. As in prior years, NAIC 1 allocations decreased, while NAIC 2 allocations increased, albeit at a lower rate than prior years.

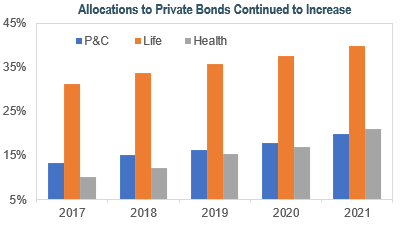

- Allocations to privates continued to increase in 2021 as insurers sought out additional yield. As rates potentially rise further and the economy continues to face a number of headwinds in 2022, it will be interesting to see if the trend remains.

- We believe insurers may move up in quality and back into public bonds given they no longer need to stretch as far as they did the past few years to achieve their desired yield target. Given the volatile environment, maintaining the liquidity of public bonds may also be in favor.

- Additionally, for some insurers, high-yield (HY) bonds, specifically higher-quality HY, may offer attractive value following the changing Risk-Based Capital (RBC) factors that provide more favorable capital treatment.

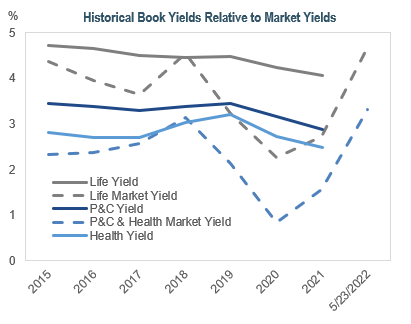

Fixed Income Observations Spotlight: Book Yields – Bottomed Out, But On The Rise

- Despite the increase in rates in 2021, book yields on insurance company fixed income investment portfolios continued to decline and hit an all-time low at year-end.

- With the continued increase in rates and high levels of inflation, book yields should improve in 2022 as reinvestment rates are largely higher than current book yields on bond portfolios, thus insurers should be able to reinvest cash flows at higher rates.

- In this rising rate environment, we believe insurers should consider relative value trades to allow for improvement in book yield and potential future total return while optimizing gains and losses in the process. However, making such shifts could be difficult without realizing losses given how much rates have risen this year.

- It is important for investment managers to maintain frequent communication with insurers to avoid any surprises and negative accounting impact from portfolio turnover.

IR+M’s Take On 2022 & Opportunities in a Rising Rate Environment

- As the environment shifts from one of depressed book yields to one of rising rates and higher inflation, we believe there are ways we can partner with insurers to help optimize their investment portfolios.

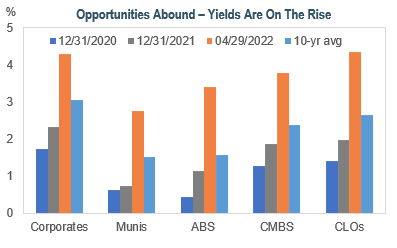

- Higher yields and wider spreads create divergence and opportunities across corporates, munis, and the securitized sector. Year-to-date, yields have risen almost 2% across sectors and are well-above both the trailing 5- and 10-year averages.

- Corporates: Fundamentals continue to be strong so the risk of impairments should remain relatively low. The yield differential between investment grade and HY has widened which may entice insurers to increase allocations to HY especially given the changing RBC factors for life companies.

- Munis: With the rise in yields and muni/Treasury ratios, munis present an attractive relative value opportunity, especially since the value of the tax exemption has grown with the higher rate environment. Munis are also broadly insulated from geopolitical crises and have generally outperformed other spread products during volatile and uncertain market environments.

Securitized:

- Asset-Backed Securities (ABS) (Non-traditional): We favor several non-traditional ABS subsectors such as Whole Business, Datacenters, and Single-Family Rentals. We believe these subsectors offer insurers attractive spreads, yields, and capital treatment. These sectors also provide diversification benefits and strong structural protections.

- Utility Rate Reduction ABS Bonds: Given the positive social aspects of these bonds, we rate this subsector highly from an ESG perspective. The securitization results in the lowest cost passed on to the ratepayer and low-income customers are often exempt from paying. In addition to having positive ESG aspects, issuance has picked up in 2022.

- Commercial Mortgage-Backed Securities (CMBS) (Vintage Conduit): We believe this sector provides insurers with a diversified, up-in-quality approach as it offers value in the short end given enhanced credit protection with minimal prepayment volatility.

- Collateralized Loan Obligations (CLOs): CLOs provide attractive relative value, particularly within the AAA-rated tranches. The structural strength of CLOs has proven out over multiple credit cycles and the floating nature of CLOs should shield insurers from rate volatility.

At IR+M, we believe the current environment presents investment opportunities for insurers to improve portfolio quality and book yield. We believe that bottom-up security selection is paramount in this environment, especially since realized losses can occur as rates rise and bond prices fall. Through our experience managing high quality fixed income portfolios and partnering with insurance clients, we think we are well-positioned to help fulfill investment needs across a variety of rate and spread environments, while optimizing book yield and limiting financial statement volatility.