My paternal grandfather grew up on a farm in Elkhart, Kansas. Willing to do anything to get off the farm, he joined the Navy, went through flight school, became a pilot, and fought in the Korean War. Later in life, he started sharing some of his stories, from purposely getting sprayed by a skunk at age 10 so he could miss school to war anecdotes. He was strong, brave, kind, compassionate, principled, and in my eyes, as Randy Travis put it, he walked on water. He was the greatest man I’ve ever known. After the Navy, Granddaddy went on to be a commercial pilot for Eastern Airlines. He saw most of the world, cherished cultures, and loved life. Despite all he experienced, the one thing he missed most was life on the farm. Granddaddy enjoyed flying at night. When flying over one area, he noticed that it was always pitch black — not a light around. No lights mean a rural area. Grandaddy asked the navigator what the town below was, and the response was Danielsville, GA. After flying over the site many times over the subsequent months, Granddaddy got in his truck, drove to Danielsville, and found a farm for sale. That 172-acre parcel would become the greatest gem of my childhood. Amazing to think that because of the dark, he found a gem.

2020 has certainly had some dark moments. In these moments, much as we have in previous dark times, we found some gems. Opportunities are most abundant in the dark, since only those who are willing to dig can unearth the gems — some new, and some that others discarded along the way. Of all the glittering stones and opportunities that we have found in 2020 to add to the portfolios, many of my favorites have been in the form of taxable munis.

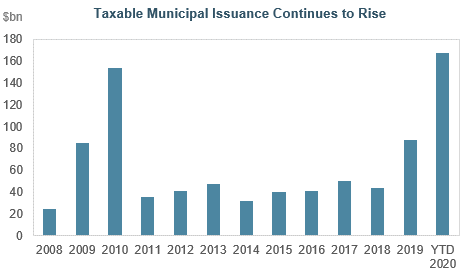

The taxable muni market has certainly evolved and matured over the last decade, more than tripling in size since its pre-Build America Bond (BABs) days of 2009-2010, expanding the number and types of issuers, embracing institutional buyers’ unwillingness to accept issuer-friendly convexity structures without adequate spread compensation, and, most recently, filling out the yield curve with new short and intermediate offerings. While we are likely nearing the point where a diversified all taxable-muni portfolio can be created, we continue to view taxable munis as most beneficial and value-enhancing when part of a well-diversified portfolio, as opposed to in isolation.

Taxable munis comprise over 15% of the total municipal market, versus less than 5% prior to the BABs program. With 2020 issuance approaching $200bn, and the potential to exceed that amount in 2021, we expect the market to continue to attract buyers and become an ever-growing segment of portfolios, especially where ratings’ constraints exist. The average rating in the investment-grade municipal market is Aa3 compared with Baa1 in the intermediate corporate market. These higher ratings, which are often coupled with slightly enhanced yields compared to single-A corporates, can improve capital allocation relative to yield for insurance and other regulated investors. For some investors, in a low-yield, low corporate tax rate environment, taxable munis may offer greater after-tax yields than tax-exempt bonds of the same issuer, depending on the part of the curve. More interestingly, in our crossover strategy, we sometimes buy the longer exempts, where the value of the exemption is maximized and liquidity not compromised, and the shorter taxables, where the value of the exemption is least, and own both in smaller weights. This highlights the value that can exist when getting between the wall and the wallpaper (or in between rocks for our gem analogy) and quantifying every part of the after-tax proposition.

Investors often assume smaller taxable muni cusips suffer from a liquidity perspective, and to that, we say “it depends.” Longer taxables, meaning those that exceed ten years to maturity, do have very pronounced differences in liquidity between index-eligible (greater than $300mm cusip size) deals and those that do not meet index eligibility requirements. In the longer-end, selectivity and liquidity premiums must be measured twice. Shorter and intermediate cusips, however, do not suffer from these same binary eligibility factors. That is, smaller deals and cusips can remain adequately liquid despite their size. This blanket perception of liquidity, coupled with some smaller deals not being worth others’ time and resources, leaves overlooked gems, many of which we have sifted through and added to the portfolios this year.

The last, but not least, polish that makes the taxable muni gem shine so bright is ESG. The municipal market is a haven for positive ESG issuers. From infrastructure to education, green power to non-profit hospitals, and low-income housing to municipalities whose governance structure represents the will of the people through a democratically-elected process, the municipal market shines bright in the realm of ESG. As ESG continues to become a focal point for many investors, we feel the taxable municipal market will continue to offer additional areas of sparkle for relative value in a portfolio.

2021 is likely to bring us the largest amount of taxable muni issuance ever, and the market could pass $1 trillion only a few years from now. As this market continues to evolve, and pricing and trading mechanics continue to offer value, we remain committed to identifying and delivering value in the space.

For our clients who have been with us through these and other dark times, we will always endeavor to unearth a few gems when the lights go out. Rest assured, we are not flying in the dark.