Prior to the coronavirus pandemic, the global green bond market was experiencing significant momentum and gaining traction in the US. As the market grappled with the impact of the crisis, the focus shifted to social and sustainability bonds, making these so-called “use-of-proceeds” bonds more mainstream. Despite their recent surge in popularity, they have yet to be as widely accepted – and issued – as green bonds. In this piece, we discuss various use-of-proceeds bonds, look at the green bond universe, and outline key investor considerations.

SURVEYING THE LANDSCAPE

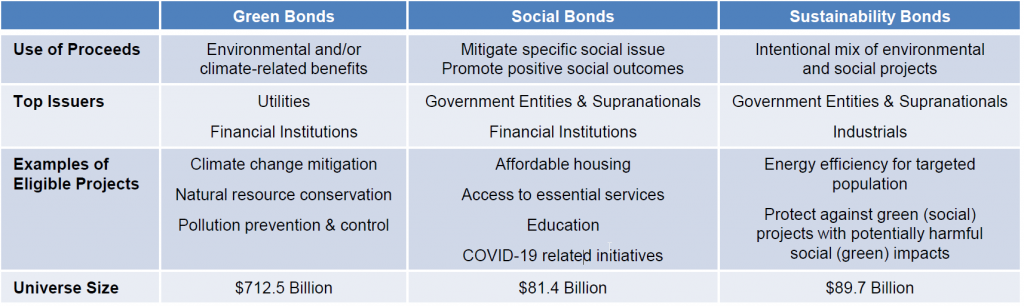

- Green, social, and sustainability bonds designate a specific use for the proceeds raised and are the most widely issued.

- Sustainability-linked, Sustainable Development Goal (SDG)-linked, and other key performance indicator (KPI)-linked bonds have emerged recently, where proceeds are most often allocated to general corporate purposes but the coupon is increased if the indicated targets are not met. This provides a monetary incentive for issuers to follow through on stated goals.

- Transition bonds are the newest members of the sustainable bond group and are meant to help carbon-intensive (“brown”) companies facilitate a shift toward long-term environmental goals. These can be tied to targeted use of proceeds or overall company goals. As a more recent addition to the market, skepticism remains and some question the need to distinguish a transition bond from a green bond, while others view it as a more credible label.

Green bond issuance increased considerably after the International Capital Market Association (ICMA) developed and promulgated its voluntary Green Bond Principles (GBPs) in 2014. S&P Global Research estimates that 80-90% of green bond issuance is now aligned with the GBPs. ICMA also maintains voluntary Social Bond Principles and Sustainability Bond Guidelines to help promote transparency, disclosure, and reporting. Fears of “greenwashing” and “social-washing” remain, but the increased alignment with the GBPs in particular provides investors comfort and the ability to audit the actual use of proceeds for green bonds. We expect social and sustainability bonds to follow.

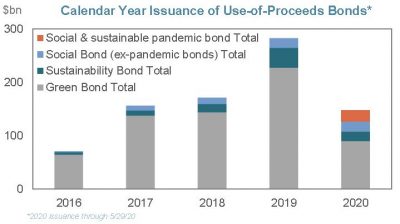

Green bond issuance hit an all-time high in 2019, as over 400 issuers came to market with a focus on alternative energy, green buildings, sustainable transport, and energy efficiency projects. As the market continues to grow and diversify, investors are becoming more comfortable investing in green bonds.

Green bond issuance hit an all-time high in 2019, as over 400 issuers came to market with a focus on alternative energy, green buildings, sustainable transport, and energy efficiency projects. As the market continues to grow and diversify, investors are becoming more comfortable investing in green bonds.

Social factors have generally been the most difficult to measure. Issuance has typically trailed that of green bonds. However, 2020 green bond sales are down 12% compared to this time last year and social and sustainability bonds have more than doubled.

GOING GREEN

- For green bond issuers, reporting and documentation requirements can be cumbersome. However, the burgeoning benefits, such as ability to market, expand their investor base, improve their company’s image, and potentially lower their cost of borrowing, can outweigh these drawbacks, particularly if they are repeat issuers.

- Many smaller companies and municipalities are less likely to issue green bonds given the additional hurdles.

- While the use-of-proceeds bond market is growing and expanding to different sectors, potential liquidity concerns remain, given the large buy-and-hold investor base and relatively small universe size.

- The escalated interest in green bonds, as investors search for tangible impact from their dollars, has supported liquidity within the space. On average, green bonds have tighter bid/ask spreads than the broader investment grade corporate index and overall green bond turnover and liquidity – particularly during the recent volatility – was similar to the broader market.

- The escalated interest in green bonds, as investors search for tangible impact from their dollars, has supported liquidity within the space. On average, green bonds have tighter bid/ask spreads than the broader investment grade corporate index and overall green bond turnover and liquidity – particularly during the recent volatility – was similar to the broader market.

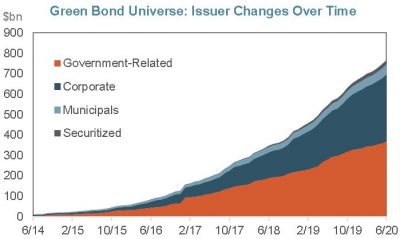

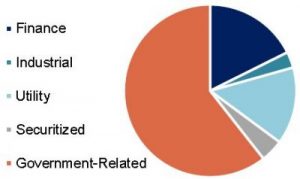

- The green bond market has expanded from a majority of government-related issuance to include significant issuance by corporations. When compared to the overall US investment grade market, green bonds are comprised of higher credit quality issuers with shorter maturity bonds and is highly concentrated in particular sectors, such as Utilities and Financials.

- How do green bond returns stack up? When adjusting for the duration, credit quality, and overall sector diversification discrepancies, recent studies have shown that performance for most green bonds is aligned with their non-green equivalents and have similar transaction costs.

GREEN DOESN’T ALWAYS MEAN GO

Fundamental research needed: At IR+M, we believe that fundamental research is needed regardless of the bond’s label. The overall credit profile, bond structure, and relative value assessment drive all of our investment decisions.

Additional due diligence may be necessary: Particularly as many focus on “building back better” after the pandemic, the use-of-proceeds bond market may experience a surge of issuance and added due diligence will be required to protect against green- or social-washing.

Beware the lack of diversification: Although expanded recently, the green bond universe still lacks sector diversification. Passive exposure to ESG strategies, through a green bond index, may result in unintentional sector overweights or underweights relative to the broader market.

Beware the lack of diversification: Although expanded recently, the green bond universe still lacks sector diversification. Passive exposure to ESG strategies, through a green bond index, may result in unintentional sector overweights or underweights relative to the broader market.

- We believe that active management, to ensure rigorous credit analysis and overall portfolio allocation, is crucial to delivering strong risk-adjusted returns.

While we are encouraged by the growth, increased transparency, and performance of the green, social, and sustainability bond universe, we remain committed to our bottom-up approach and bond-by-bond analysis. We believe that no matter how a bond is labeled, rigorous fundamental research is needed and we continue to evaluate the credit holistically, based on fundamentals and material ESG factors, and an assessment of relative value.